The 3 Layers of Retirement Income

What Are the 3 Layers of Retirement Income? (Quick Answer)

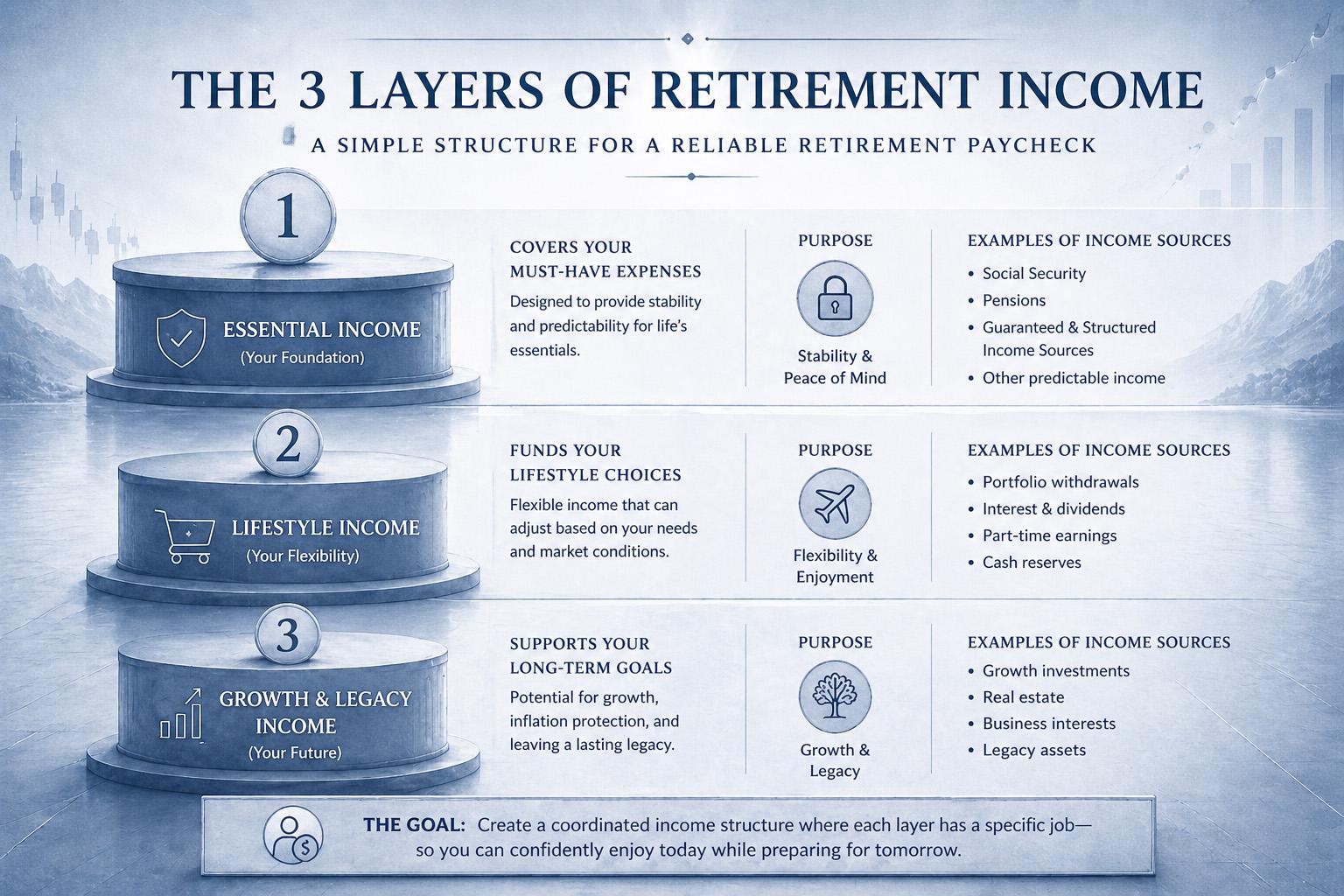

- Essential income (core expenses)

- Lifestyle income (flexible spending)

- Growth & future income (long-term needs)

Why Structuring Income Into Layers Changes Everything

- Moves away from one “bucket” thinking

- Aligns income with real-life spending

- Reduces pressure on investments

This layered approach is a central concept within Income Architecture in Retirement: How to Build a Reliable Paycheck for Life, where income is organized into distinct roles rather than treated as a single pool.

Layer 1 – Essential Income (Your Foundation)

What This Layer Covers

- Housing, food, and healthcare

Key Characteristics

- Predictable

- Stable

- Not dependent on market timing

Where Predictable & Structured Income Fits

Some income sources within this layer are designed to provide more consistent and structured cash flow, helping cover essential needs regardless of market conditions. This role is explored further in The Role of Predictable and Structured Income in Retirement.

Layer 2 – Lifestyle Income (Flexibility Layer)

What This Layer Supports

- Travel, hobbies, discretionary spending

Why Flexibility Matters

- Adjust to changing conditions

- Reduces pressure during volatility

Layer 3 – Growth & Future Income (Longevity Layer)

Purpose of This Layer

- Long-term growth

- Inflation protection

Why It’s Not Used Immediately

- Allows assets to compound

- Avoids unnecessary withdrawals

How the 3 Layers Work Together

- Foundation = stability

- Flexibility layer = adaptability

- Growth layer = longevity

Structuring income this way is what allows financial resources to be translated into a more consistent paycheck, as discussed in How to Turn Your Portfolio Into a Paycheck.

Common Mistakes When Structuring Income

- Treating all assets the same

- Over-reliance on growth asset

- Ignoring income roles

Conclusion

Structuring income into layers creates clarity and usability—making retirement income easier to understand and more adaptable over time.