Income Architecture in Retirement: How to Build a Reliable Paycheck for Life

Most people spend decades building their savings—but far fewer know how to turn them into income.

As retirement approaches, the question shifts from:

“How much have I accumulated?”

to

“How do I turn this into something I can live on?”

This is where uncertainty often begins.

Because retirement isn’t just about investments—it’s about income.

That’s where a structured approach—Income Architecture—helps bring clarity. It’s not about adding complexity. It’s about organizing what you already have into a system that supports your life.

What Is Income Architecture? (In Plain English)

Income Architecture is a way of organizing financial resources so they can consistently support your lifestyle.

Instead of relying on one portfolio to do everything, your income is structured into distinct roles, each with a clear purpose.

Think of it like building a home:

- A foundation that provides stability

- A structure that gives flexibility

- A top layer that supports long-term growth

The objective isn’t just to generate returns—it’s to create reliable, usable income.

This structured way of thinking builds on the principles behind the Retirement Income Coordination Framework™.

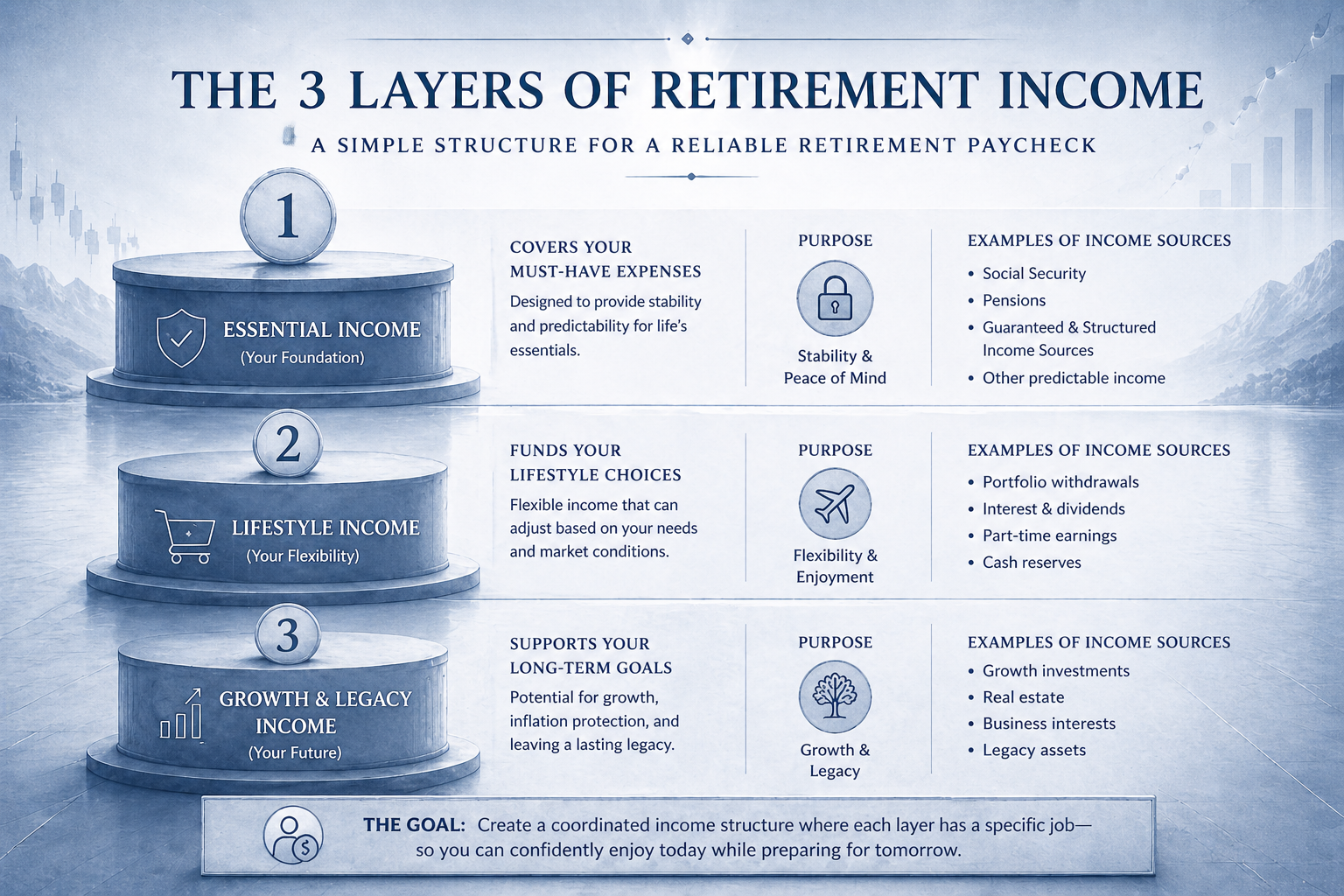

A Simple Way to Visualize Retirement Income

Rather than relying on a single pool of assets, income is divided into three coordinated layers, each designed to perform a specific role.

The 3 Layers of Retirement Income

Layer 1 – Essential Income (Your Foundation)

This layer is designed to cover must-have expenses, such as:

- Housing

- Food

- Insurance

- Healthcare

The goal here is predictability and stability.

Common sources include:

- Social Security

- Pensions

- Structured or predictable income sources

When this layer is secure, it creates a baseline of confidence—core needs are covered regardless of market conditions.

Layer 2 – Lifestyle Income (Your Flexibility Layer)

This layer supports the things that make retirement enjoyable:

- Travel

- Dining

- Hobbies

- Personal interests

Unlike essential income, this layer is inherently flexible.

It can adjust based on:

- Market conditions

- Personal priorities

- Life changes

This flexibility allows for enjoyment without placing unnecessary strain on long-term resources.

Layer 3 – Growth & Legacy (Your Future Layer)

This layer is focused on the future.

It’s designed to:

- Support long-term growth

- Help offset inflation

- Provide for future needs or legacy goals

Because it’s not relied on for immediate income, it can remain invested for longer-term opportunities.

Quick Answer: What Are the Three Layers of Retirement Income?

A structured approach that divides income into:

- Essential expenses

- Flexible lifestyle spending

- Long-term growth resources

Turning Your Savings Into a Retirement Paycheck

A common misconception is that a portfolio will naturally translate into income.

In practice, income requires deliberate structure.

Without it, withdrawals may become inconsistent or influenced by short-term conditions.

Why a Portfolio Alone Isn’t Enough

- Investment values fluctuate

- Spending needs tend to remain ongoing

- Timing of withdrawals can influence long-term outcomes

Organizing resources into defined roles helps align them with how income is actually used.

Creating Consistent Cash Flow

A structured approach connects different income sources to specific purposes:

- Stable sources aligned with essential needs

- Flexible sources aligned with discretionary spending

- Long-term assets reserved for future use

This can create a more consistent and predictable flow of income over time.

Protecting Against Market Timing Risk

One of the key risks in retirement is not just market performance, but the timing of that performance.

Periods of decline early in retirement can have a greater impact when withdrawals are required.

Structuring income sources can help:

- Reduce reliance on market conditions for essential expenses

- Limit the need to draw from long-term assets during unfavorable periods

This is often referred to as sequence of returns risk, which can affect how income unfolds over time.

Why Simple Rules (Like the 4% Rule) Can Fall Short

Rules of thumb are often based on generalized assumptions, such as:

- Fixed spending levels

- Consistent market behavior

- Uniform time horizons

In reality, conditions and spending needs evolve.

A structured approach allows for adjustments over time, rather than relying exclusively on static guidelines.

This concept is explored further in Why the 4% Rule Creates More Risk Than You Think, where the limitations of fixed withdrawal strategies and their impact on long-term income are examined in greater detail.

The Role of Structured and Predictable Income Sources

Some income sources are designed to provide consistent payments regardless of market conditions.

Within Income Architecture, these are typically aligned with the essential income layer.

Key Characteristics

- Predictable income

- Reduced reliance on withdrawals

- Support for essential expenses

- Trade-offs may include flexibility or liquidity

Quick Answer: Do You Need Predictable Income in Retirement?

Some prioritize stability through predictable income sources, while others rely more on flexibility.

The right approach depends on how income is structured overall.

Don’t Overlook Taxes—They Affect What You Actually Keep

Income isn’t just about what is generated—it’s about what remains after taxes.

Key considerations include:

- Timing of withdrawals

- Account types (taxable, tax-deferred, tax-free)

- Long-term tax efficiency

These factors directly influence real income.

A Structure That Adjusts With You

Retirement isn’t static—income shouldn’t be either.

An effective structure allows for:

- Adjustments based on conditions

- Changes in spending

- Evolving priorities

Flexibility keeps income aligned with real life.

This idea is closely tied to what’s known as a retirement spending strategy—how income adjusts over time to reflect changing needs, rather than remaining fixed.

Quick Answer: How Do You Make Retirement Income Last?

By balancing:

- Stable income sources

- Flexible spending

- Long-term growth assets

—while adjusting as conditions evolve.

Common Mistakes to Avoid

- Using accumulation strategies during retirement

- Relying only on fixed withdrawal rules

- Ignoring timing risk

- Not assigning roles to assets

- Focusing only on returns instead of usable income

Bringing It All Together

Income in retirement is shaped by how resources are organized.

A structured approach provides:

- Clarity around income sources

- Alignment with spending needs

- Flexibility over time

Conclusion

As retirement approaches, the focus shifts from accumulation to income design.

Organizing resources into clearly defined roles makes that transition more understandable—and more manageable.

A structured approach like Income Architecture helps create a clearer path toward consistent, reliable income.

FAQs

What is income architecture in retirement?

A method of organizing financial resources into structured roles to support consistent income.

How do you turn investments into income?

By aligning different assets with specific income functions rather than relying on unstructured withdrawals.

What are the safest retirement income sources?

Sources with predictable or contract-based payments are generally considered more stable.

Do you need predictable income in retirement?

It depends on how income is structured—some prioritize stability, others flexibility.

How do you protect income from market downturns?

By separating essential income from market-dependent assets.

What is a sustainable withdrawal approach?

One that balances income needs, market conditions, and long-term preservation.