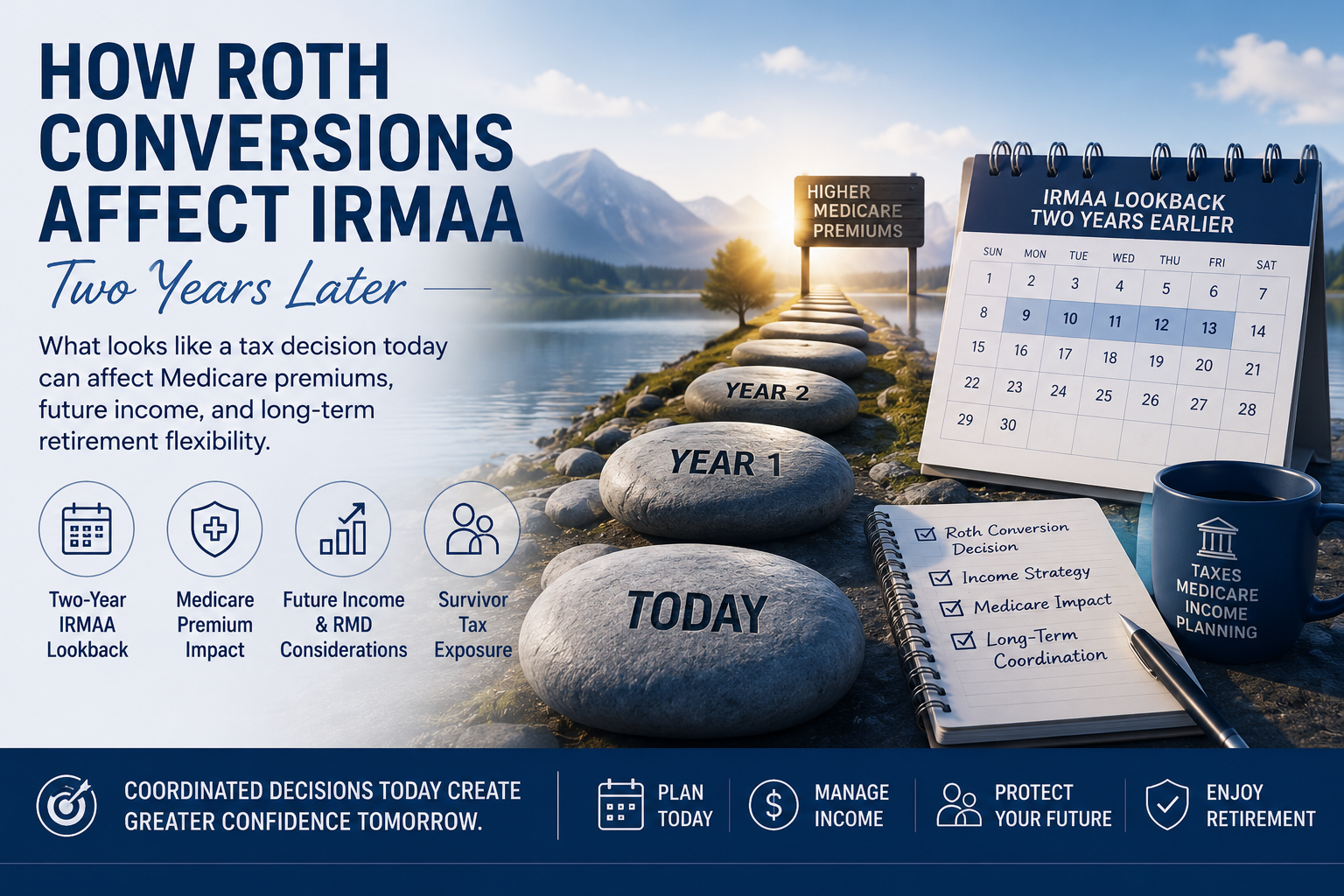

How Roth Conversions Affect IRMAA Two Years Later

Many retirees focus on the immediate tax impact of Roth conversions but overlook how those decisions can affect Medicare premiums two years later through IRMAA income calculations.

Many retirees focus on the immediate tax impact of Roth conversions but overlook how those decisions can affect Medicare premiums two years later through IRMAA income calculations.

Many couples expect retirement to happen all at once. In reality, one spouse often retires years before the other. This article explores how staggered retirement can affect taxes, healthcare coverage, spending patterns, Social Security timing, and long-term household financial coordination.

Explore how predictable and structured income fits into retirement and supports essential expenses within a balanced income framework.

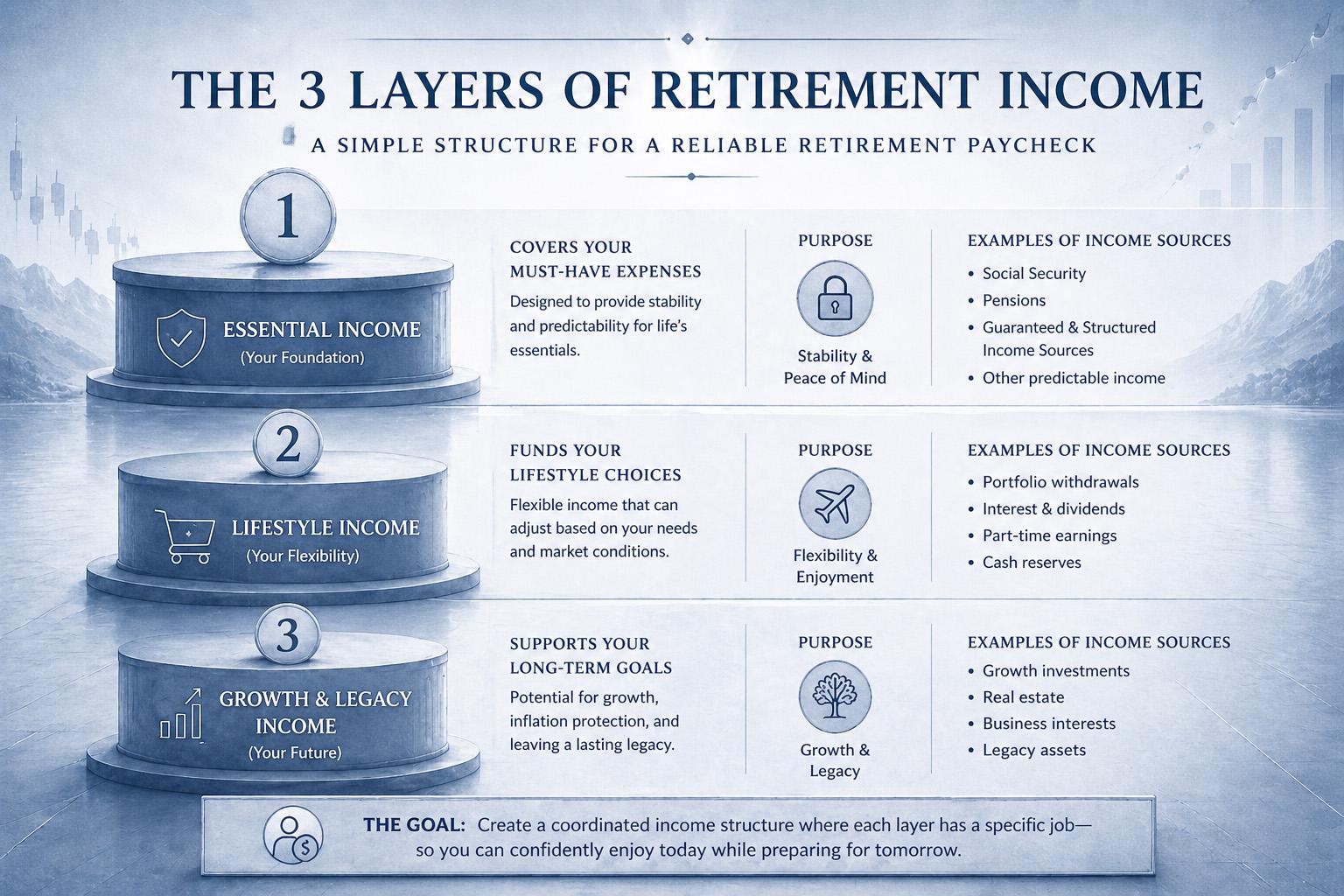

Understand the 3 layers of retirement income and how structuring income into defined roles can help create stability, flexibility, and long-term growth.

Learn how to turn your savings into a reliable retirement paycheck using a simple, structured income strategy designed for long-term clarity and confidence.

The 4% rule is often seen as a safe withdrawal strategy—but it may introduce more risk than it removes. By relying on a fixed percentage, it ignores how markets behave, how spending evolves, and how decisions are made over time. A more effective approach focuses on defining sustainable spending with flexible guardrails rather than rigid rules.