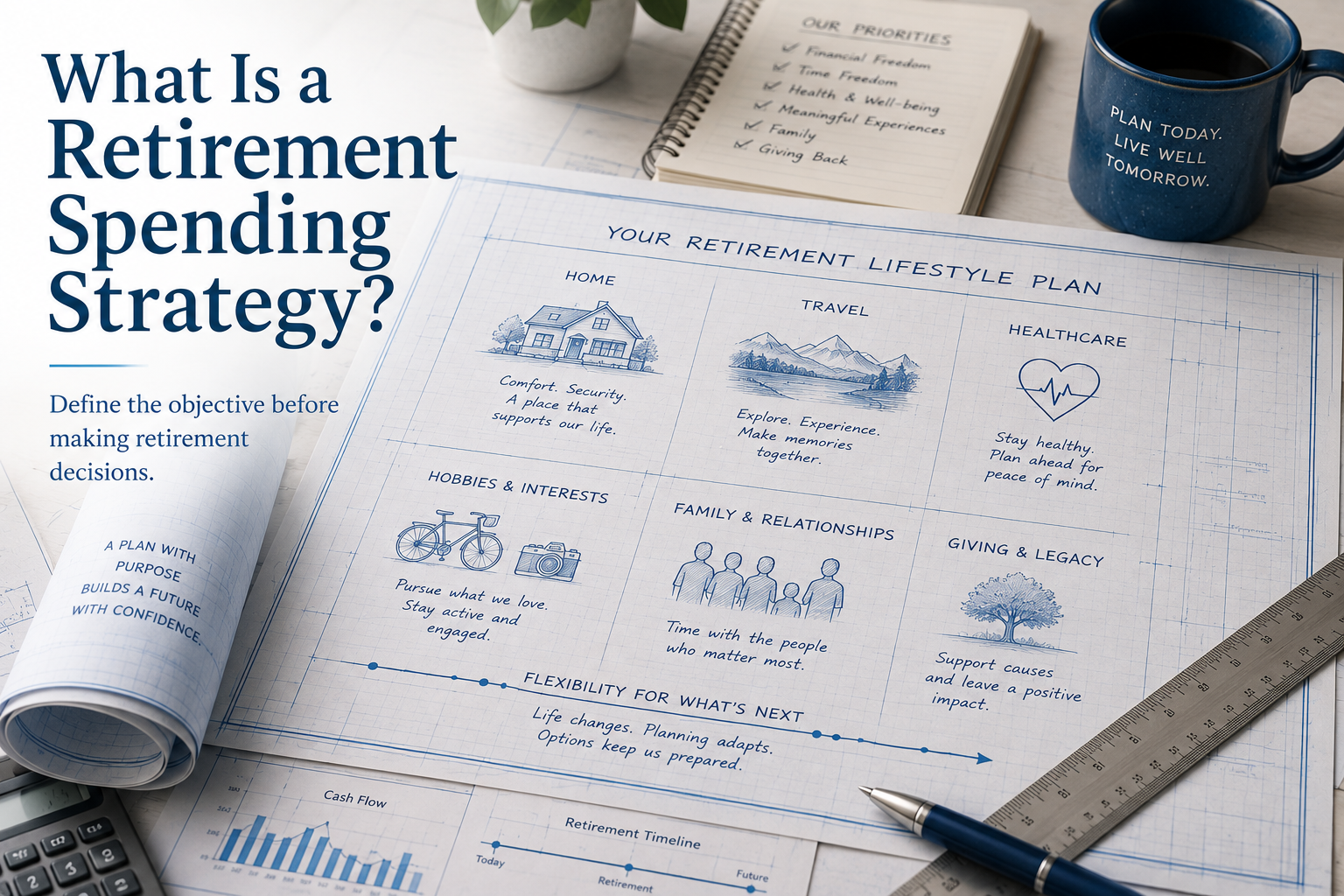

What Is a Retirement Spending Strategy?

A retirement spending strategy is more than estimating expenses or choosing a withdrawal rate. It defines the spending your retirement resources are intended to support and establishes the foundation for coordinating income, taxes, and investments throughout retirement.