Retirement Is a Coordination Process

Retirement is not a portfolio strategy.

It is a decision system.

Spending, income, taxes, and investments do not operate independently. Each decision affects the others. When managed separately, even well-intentioned choices can work against each other.

The Retirement Coordination Framework™ brings these moving parts together into a single decision-making process.

Because retirement outcomes are shaped not only by investment returns, but by how decisions are coordinated over time.

The Coordination Problem

Many retirees unknowingly manage retirement in pieces:

- Spending decisions made without considering their long-term income implications

- Income decisions evaluated independently of taxes

- Tax decisions made one year at a time

- Investment decisions managed without considering spending responsibilities

Each decision may be reasonable on its own.

But without coordination, they can work against each other.

- Withdrawals can increase taxes and Medicare premiums

- Tax decisions can reduce long-term flexibility

- Spending can drift out of alignment with available resources

- Investment decisions may not reflect withdrawal needs or sequence-of-returns risk

The issue is not a lack of knowledge.

It is a lack of coordination.

What is needed is a structured way to evaluate these decisions together and revisit them as circumstances evolve.

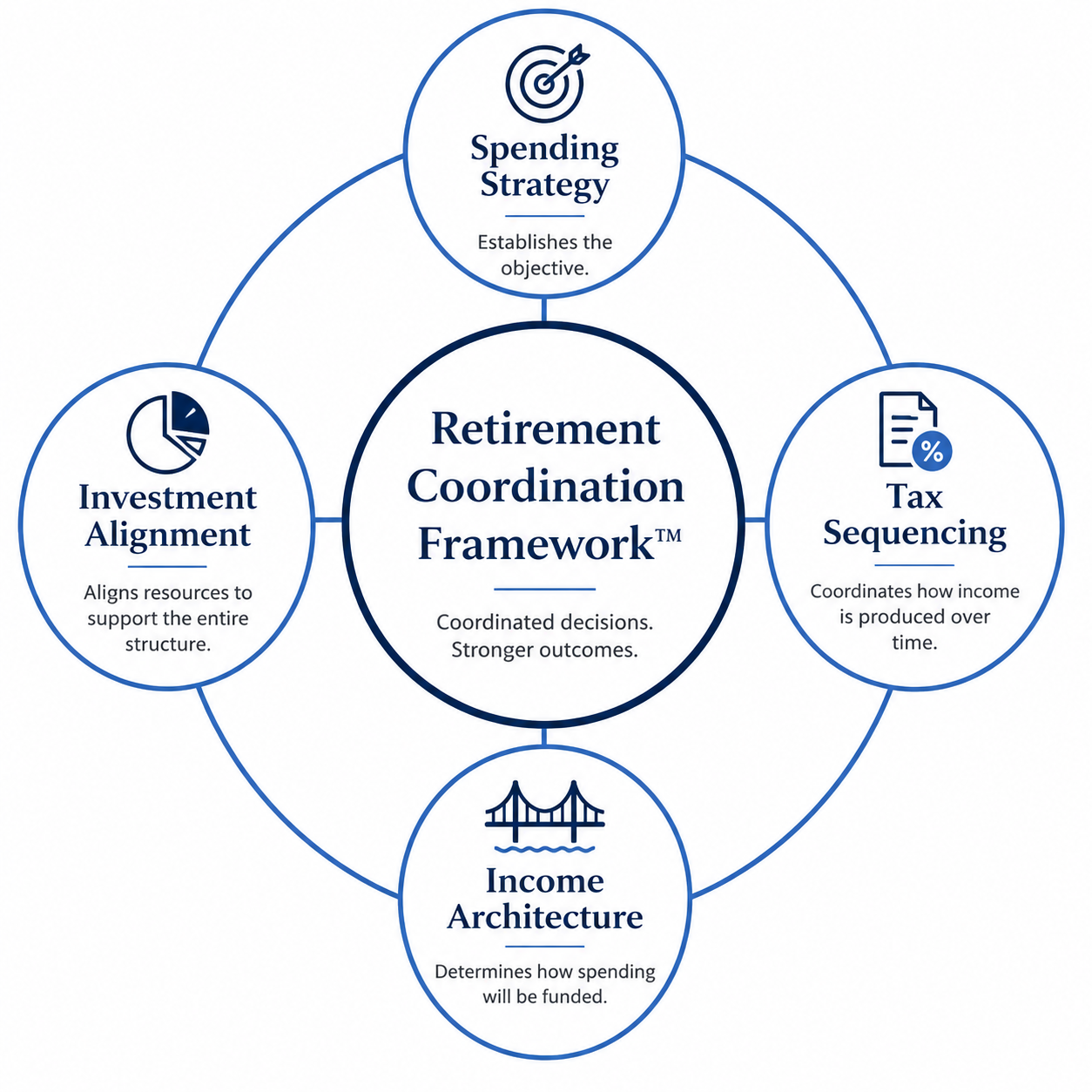

The Retirement Coordination Framework™

1. Spending Strategy

Spending establishes the objective.

Once spending has been defined, income can be structured to support it.

That income structure creates tax decisions.

Investment decisions are then made in support of the entire structure.

Coordination begins with the spending decision.

Spending establishes the objective.

2. Income Architecture

Income architecture transforms your spending strategy into a practical income structure.

Once spending has been defined, the next question becomes:

Which retirement resources should provide that income, when should they be used, and how should they work together over time?

Income architecture coordinates:

- Guaranteed income sources

- Portfolio withdrawals

- Cash reserves

- Distribution sequencing

- Flexibility to adapt income as retirement evolves.

The objective is not simply generating income.

It is creating an income structure that supports spending while providing flexibility for future tax and investment decisions.

Income transforms objectives into a practical retirement paycheck.

3. Tax Sequencing

Once an income structure has been established, tax decisions help determine how that income is produced as effectively as practical.

We evaluate:

- Social Security timing

- IRA, Roth, and taxable account sequencing

- Capital gains realization

- Medicare premium thresholds

- Multi-year tax bracket management

The objective is not to minimize taxes in a single year.

The objective is to make income and tax decisions that support spending needs and future flexibility over time.

Taxes shape how income is delivered over time.

4. Investment Alignment

Investment decisions support the retirement structure.

They do not define it.

Once spending has been established, income has been structured, and tax considerations have been evaluated, the remaining question is:

Which retirement resources are best suited to support each responsibility?

Investment alignment begins by assigning responsibilities to retirement resources.

Some retirement resources may be intended to support near-term spending.

Others may primarily support long-term growth, tax flexibility, or legacy objectives.

Only after those responsibilities are understood are investment decisions made.

Asset allocation, risk management, rebalancing, and asset location are evaluated within the context of:

- Spending strategy

- Income architecture

- Tax sequencing

The objective is not simply to build a diversified portfolio.

It is to align each retirement resource with the responsibility it serves within the overall retirement structure.

Performance matters.

Purposeful alignment matters more.

Investments support the retirement structure—they don't define it.

Retirement Is Coordinated from the Spending Decision Forward

Many retirement planning approaches begin by building an investment portfolio.

Within the Retirement Coordination Framework™, the sequence is intentionally reversed.

Spending establishes the objective.

Income architecture determines how spending will be funded.

Tax sequencing coordinates how income is produced over time.

Investment alignment positions retirement resources to support the entire structure.

Each decision builds on the one before it, creating a coordinated system rather than a collection of independent strategies.

Investment Within a Retirement System

In many planning approaches, investments lead.

Within the Retirement Coordination Framework™, investments are managed in support of spending, income, and tax decisions—not independently of them.

Rather than asking,

"What portfolio should I own?"

the framework first asks,

"What responsibility does each retirement resource serve?"

Only then are investment decisions made.

Taxes as a Structural Constraint

Taxes influence retirement outcomes more than many retirees expect.

Income and withdrawal decisions, tax brackets, Medicare-related thresholds, and future flexibility are evaluated together.

Decisions are made deliberately—not reactively.

Oversight Over Time

Coordination is not a one-time event.

Markets shift.

Tax laws change.

Spending evolves.

Life unfolds.

The framework is applied through an ongoing process of review, evaluation, and adjustment.

The objective is to support informed decision-making and sustainable spending over time.

A Coordinated System, Not Isolated Advice

The Retirement Coordination Framework™ brings spending, income, taxes, and investments together into a single decision-making process.

When these elements are evaluated together, households often benefit from:

- Better alignment across key retirement decisions

- Reduced avoidable tax exposure

- More consistent cash-flow management

- Greater clarity around trade-offs and future decisions

Retirement is not about predicting the future.

It is about coordinating decisions—intentionally and over time.