How Roth Conversions Affect IRMAA Two Years Later

Many retirees evaluate Roth conversions primarily through the lens of current taxes.

But in retirement, income decisions often continue affecting other areas of the household years later. One of the more overlooked examples is the interaction between Roth conversions and Medicare premium adjustments.

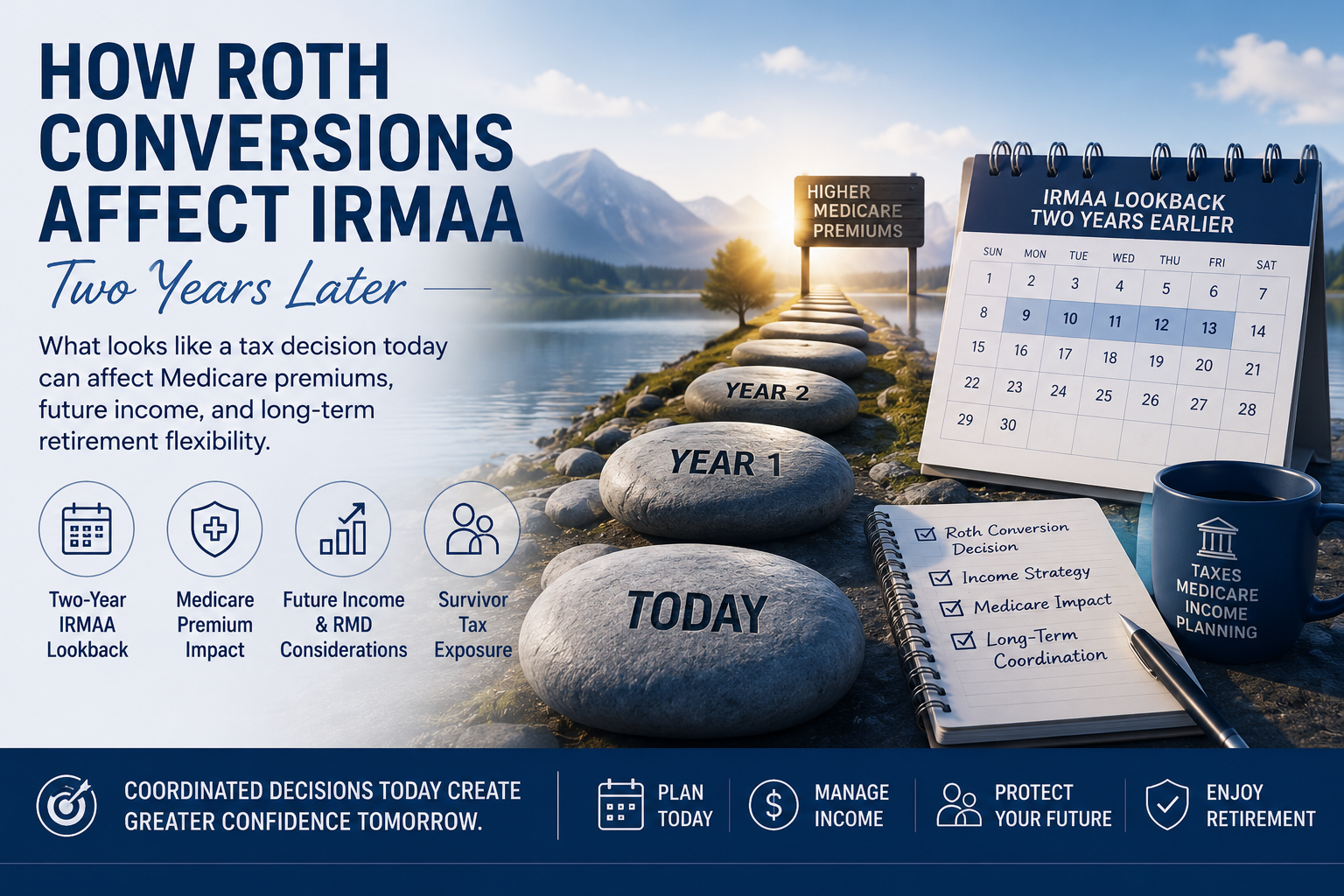

A conversion that appears manageable from a tax standpoint today can later increase Medicare Part B and Part D premiums through IRMAA rules that rely on income from two years earlier.

The issue is rarely just about whether a Roth conversion lowers future taxes. It also becomes a question of timing, income coordination, Medicare thresholds, future required distributions, and long-term household flexibility.

Why IRMAA Often Catches Retirees Off Guard

IRMAA increases Medicare Part B and Part D premiums for retirees whose income exceeds certain thresholds. The adjustment itself is not always a surprise. What often catches retirees off guard is the timing.

Many people do not immediately connect a Roth conversion completed two years earlier with a later increase in Medicare premiums. The delay can create the impression that the higher costs appeared unexpectedly, even though the original income event occurred during a prior tax year.

That disconnect becomes more noticeable in retirement because taxable income may fluctuate more than it did during working years. Withdrawals, capital gains, Social Security timing, and required distributions often begin interacting simultaneously.

A conversion that initially appeared manageable from a tax standpoint may later affect healthcare costs in ways that were less visible at the time.

Because IRMAA operates through income thresholds, even moderate increases in taxable income may affect future Medicare premiums once certain levels are crossed.

Why Roth Conversion Years Often Look Temporarily Favorable

Many retirees evaluate Roth conversions during the years between leaving full-time work and beginning required minimum distributions. Those transition years can temporarily create lower taxable income, delayed Social Security claiming decisions, and additional flexibility within certain tax brackets.

The timing can become even more layered when one spouse retires while the other continues working, since household income may fluctuate unevenly during the transition into retirement.

What initially appears to be a favorable tax window, however, often affects more than current-year taxes alone. Medicare premiums, future withdrawals, household income coordination, and long-term tax exposure may all become part of the decision later on.

Related: What Happens When One Spouse Retires Before the Other?

The Ripple Effects Often Extend Beyond Taxes

Roth conversions are often discussed as strategies for managing future tax exposure. In practice, the effects frequently extend beyond taxes alone.

Higher income from a conversion may influence Medicare premiums later through IRMAA calculations. Additional income can also affect the taxation of Social Security benefits, capital gains realization decisions, and withdrawal sequencing across taxable and retirement accounts.

Over time, these interactions may change how retirees think about future flexibility. A household that initially focused on reducing future required distributions may later begin weighing healthcare costs, spending needs, or future taxable income differently.

For some retirees, the broader objective becomes less about minimizing taxes in a single year and more about managing how multiple financial systems interact across retirement.

Related: Why Retirement Tax Planning Is Really About Timing

Why Some Retirees Reevaluate Conversions After Market Declines

Market declines sometimes change how retirees think about Roth conversions. Lower portfolio values may allow retirees to convert more shares while staying within the same tax bracket or IRMAA thresholds.

At the same time, volatility often changes how households think about liquidity and flexibility. Some retirees become more focused on maintaining cash reserves during uncertain market periods rather than increasing taxable income through additional conversions.

Emotional hesitation also becomes part of the equation. A decline may create what appears to be a more favorable conversion environment mathematically, while simultaneously making retirees less comfortable moving assets during uncertainty.

The decision often becomes less about finding the perfect opportunity and more about balancing taxes, liquidity, spending flexibility, and long-term comfort with uncertainty.

How Survivor Tax Exposure Changes the Conversation

Some Roth conversion discussions eventually shift away from current tax brackets altogether and toward future survivor planning.

After one spouse dies, the surviving spouse may still face substantial required distributions while filing taxes as a single taxpayer. That change can compress future tax brackets and potentially increase Medicare-related income adjustments later in retirement.

In that context, some households begin evaluating Roth conversions less as immediate tax decisions and more as long-term coordination decisions intended to reduce future pressure on the surviving spouse.

The tradeoffs remain complex. Current taxes may increase in exchange for greater future flexibility, lower required distributions, or different withdrawal options later on.

Why Roth Conversion Decisions Rarely Stay Static

Many retirees revisit Roth conversion decisions repeatedly over time because the surrounding variables continue changing.

Income levels shift. Spending patterns evolve. Markets fluctuate. Healthcare costs change. Tax laws eventually adjust. Household circumstances rarely remain fixed for long.

As retirement unfolds, decisions that once appeared straightforward may require reevaluation under different conditions later. A conversion strategy that looked attractive during lower-income years may feel different after required distributions begin or after healthcare costs increase.

That does not necessarily make Roth conversions right or wrong decisions. It simply reflects the reality that retirement planning is often less about isolated transactions and more about ongoing coordination across multiple systems over time.

People Also Ask

Does a Roth conversion increase Medicare premiums?

It can. Roth conversions increase taxable income in the year the conversion occurs, and Medicare premium adjustments through IRMAA are based on income from two years earlier. A larger conversion may therefore increase future Medicare Part B and Part D premiums even if income declines afterward.

How does IRMAA work after a Roth conversion?

IRMAA uses a version of modified adjusted gross income reported on tax returns from two years prior. If a Roth conversion increases income above certain thresholds, Medicare premiums may increase later based on those earlier income levels.

Why do retirees do Roth conversions before RMD age?

Many retirees evaluate conversions during lower-income years before required minimum distributions begin increasing taxable income. Those transition years sometimes create temporary flexibility within lower tax brackets.

Can Roth conversions affect a surviving spouse later?

In some cases, yes. A surviving spouse may later face higher tax exposure while filing as a single taxpayer. Some households evaluate Roth conversions partly to reduce future required distributions and improve flexibility later on.

Are Roth conversions always worth doing in retirement?

Not necessarily. The tradeoffs depend on future income expectations, Medicare implications, spending needs, tax exposure, liquidity concerns, and long-term household goals. Many retirees revisit conversion decisions multiple times over the course of retirement.

Do Roth conversions affect Social Security taxation?

They can. Because Roth conversions increase taxable income, they may temporarily increase the portion of Social Security benefits subject to taxation during the conversion year.

Conclusion

Roth conversions are often framed primarily as tax-management decisions. In retirement, however, the surrounding effects frequently extend much further.

Income decisions can influence Medicare premiums years later. Tax exposure may shift after household transitions. Withdrawal flexibility can change as spending patterns evolve. Market declines may alter how retirees think about liquidity and future income coordination.

What appears beneficial in one year may create different tradeoffs later on.

That does not necessarily make Roth conversions good or bad decisions. It simply means retirement decisions often continue interacting long after the original transaction is complete.