Withdrawal Sequencing Explained

How Retirees Pay Themselves Over Time

Once you understand that retirement income is assembled—not automatic—the next question becomes unavoidable:

Where should the money come from, and when?

Withdrawal sequencing is how retirees decide which accounts to draw from over time. It’s one of the most important—and least intuitive—parts of retirement income planning because small timing differences can quietly shape taxes, flexibility, and long-term income reliability.

What Withdrawal Sequencing Really Means

Withdrawal sequencing isn’t about picking a single “best” order and locking it in forever.

It’s about coordinating withdrawals across:

- Tax-deferred accounts (IRAs, 401(k)s)

- Tax-free accounts (Roth IRAs)

- Taxable investment accounts

- Guaranteed income sources (Social Security, pensions)

Each source affects taxes differently. Each behaves differently over time. And once withdrawals begin, those effects compound.

Why the Order Matters More Than It Seems

Two retirees can withdraw the same dollar amount and experience very different outcomes depending on which accounts fund the spending.

Withdrawal choices influence:

- Current and future tax brackets

- Medicare premiums

- Required minimum distributions later

- Flexibility when income needs change

- How resilient income remains during market stress

This is why sequencing decisions often matter more than the headline return of the portfolio.

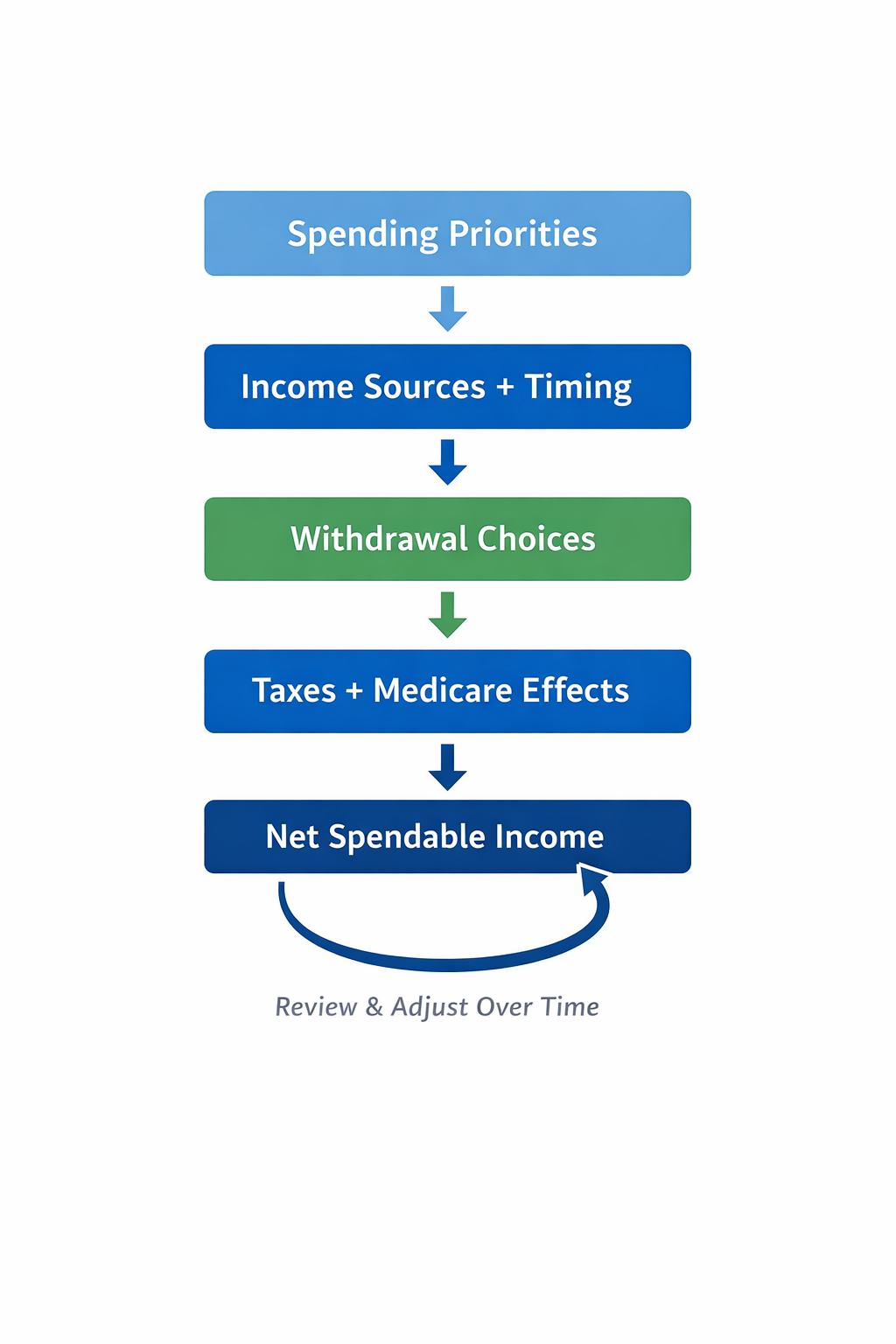

The Retirement Income Coordination Framework

Retirement works best when income, investments, and taxes are coordinated over time — not handled as separate projects. We use a simple framework: start with spending needs, map reliable income sources, coordinate withdrawal and tax decisions, and adjust as life, markets, and rules change. This approach helps keep retirement income steady and reduces surprises that often show up later.

This page focuses on how withdrawal choices across accounts shape taxes, flexibility, and long-term income reliability.

Why “Lowest Tax This Year” Can Create Problems Later

A common instinct is to withdraw in ways that minimize taxes today.

In retirement, that instinct can backfire.

Reducing taxable income early can:

- Increase required distributions later

- Push income into higher brackets down the road

- Trigger Medicare premium increases

- Reduce flexibility when circumstances change

Sequencing isn’t about avoiding taxes—it’s about shaping when and how taxes show up so income remains manageable over time.

Withdrawal Sequencing Is Dynamic, Not Static

There is no permanent “correct” sequence.

Good sequencing evolves with:

- Spending patterns

- Market conditions

- Tax law changes

- Benefit timing

- Aging and lifestyle shifts

What works in the early years of retirement may need adjustment later. The goal is not precision—it’s adaptability.

How Withdrawal Choices Affect Income Reliability

Withdrawal sequencing plays a quiet but powerful role in income stability.

Well-coordinated withdrawals can:

- Smooth taxable income

- Reduce forced withdrawals later

- Preserve optionality during market downturns

- Make spending adjustments feel deliberate rather than reactive

Poorly coordinated withdrawals often feel fine early—until flexibility disappears.

Why This Is Different From Investment Allocation

Asset allocation determines what you own.

Withdrawal sequencing determines how you use it.

Even a well-diversified portfolio can produce uneven or fragile income if withdrawals aren’t coordinated thoughtfully. This is why sequencing decisions deserve as much attention as investment structure—especially in retirement.

What a Coordinated Withdrawal Approach Changes

When withdrawals are coordinated:

- Income feels more predictable

- Taxes are easier to anticipate

- Adjustments feel incremental, not disruptive

- Trade-offs are visible before decisions are made

The result isn’t perfection. It’s control and confidence.

How This Connects to Investment Returns

Once withdrawals begin, investment returns no longer tell the full story.

What matters more is how returns interact with:

- Withdrawal timing

- Tax exposure

- Spending needs

This leads to the final anchor in the series.

→ Next: Why Investment Returns Matter Less Than Income Coordination in Retirement