Understanding IRMAA: Why Medicare Premiums Surprise Retirees

For many retirees, Medicare premiums don’t rise gradually — they jump.

And when they do, it often feels sudden, confusing, and disconnected from any recent decision.

Those jumps are usually caused by IRMAA, a Medicare surcharge that quietly ties today’s premiums to income decisions made years earlier. If you’re retired or nearing retirement, understanding how IRMAA works — and why it shows up when it does — is essential to avoiding unpleasant surprises.

What Is IRMAA?

IRMAA stands for Income-Related Monthly Adjustment Amount. It’s an additional surcharge added to Medicare premiums for people whose income exceeds certain thresholds.

IRMAA affects:

- Medicare Part B (outpatient and physician services)

- Medicare Part D (prescription drug coverage)

The key detail most retirees miss:

IRMAA is based on your income from two years earlier, not your current income.

Why IRMAA Catches Retirees Off Guard

Most people expect Medicare costs to stabilize once they stop working. IRMAA disrupts that expectation because of how and when it’s calculated.

Common reasons it surprises retirees include:

- Delayed timing — premiums today reflect income from two years ago

- Sharp thresholds — crossing a limit by even a small amount triggers the full surcharge

- One-time income events — large withdrawals, Roth conversions, asset sales, or liquidity events

- After-the-fact notice — the surcharge appears after the tax year is already closed

By the time IRMAA shows up, the decision that caused it often feels distant or forgotten.

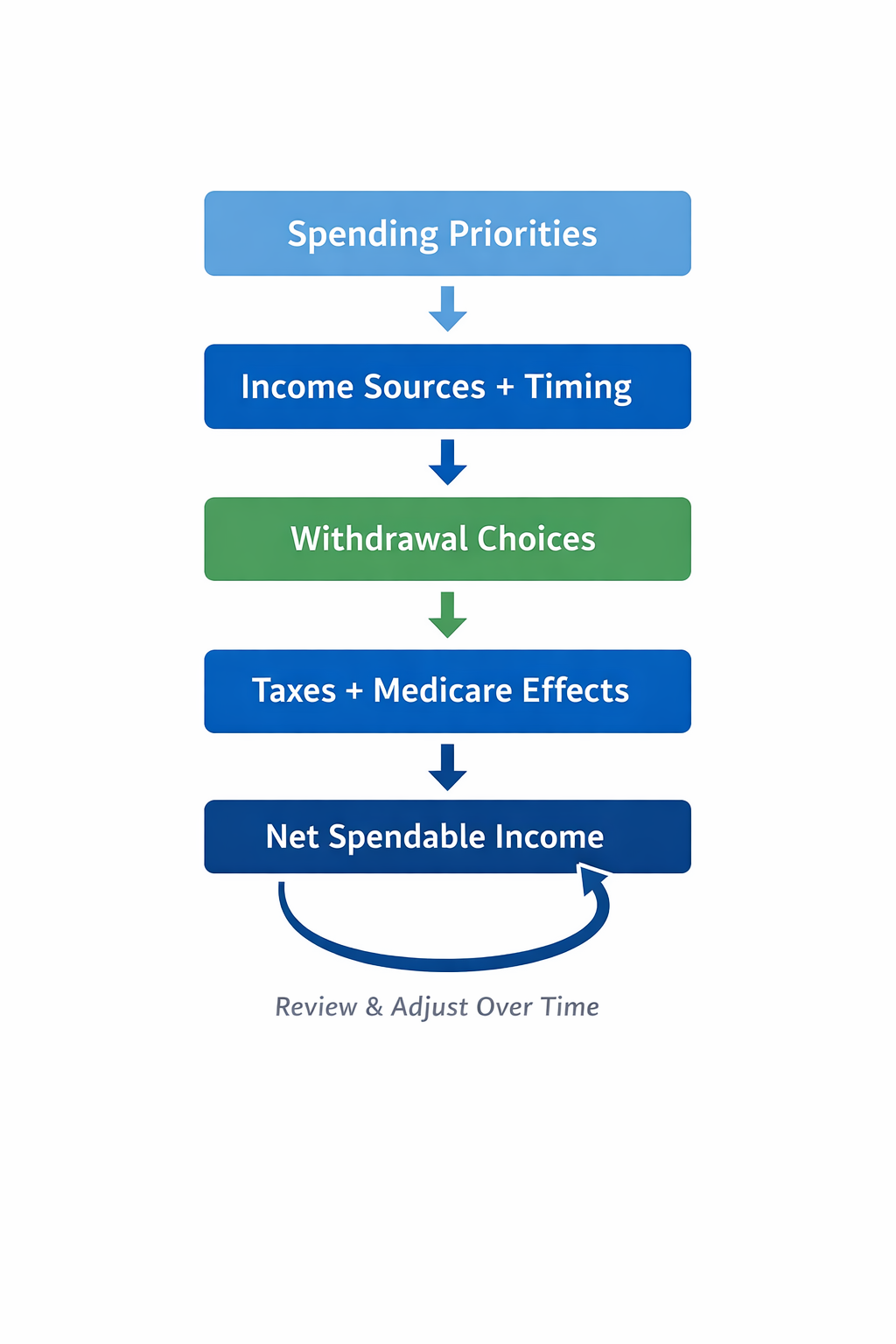

The Retirement Income Coordination Framework

Retirement works best when income, investments, and taxes are coordinated over time — not handled as separate projects. We use a simple framework: start with spending needs, map reliable income sources, coordinate withdrawal and tax decisions, and adjust as life, markets, and rules change. This approach helps reduce surprises — like unexpected Medicare premium increases — and keeps retirement spending steady and predictable.

This page focuses on how income timing and tax decisions affect Medicare premiums.

Why IRMAA Shows Up in Retirement

IRMAA isn’t triggered by everyday spending. It usually appears when income decisions stack in ways that weren’t coordinated ahead of time.

Common triggers include:

- Larger-than-expected IRA or 401(k) withdrawals

- Roth conversions concentrated into a single year

- Capital gains from selling investments or property

- Required minimum distributions layered on top of other income

- One-time liquidity events

Individually, these decisions are often reasonable. IRMAA shows up when their timing overlaps in ways that weren’t anticipated.

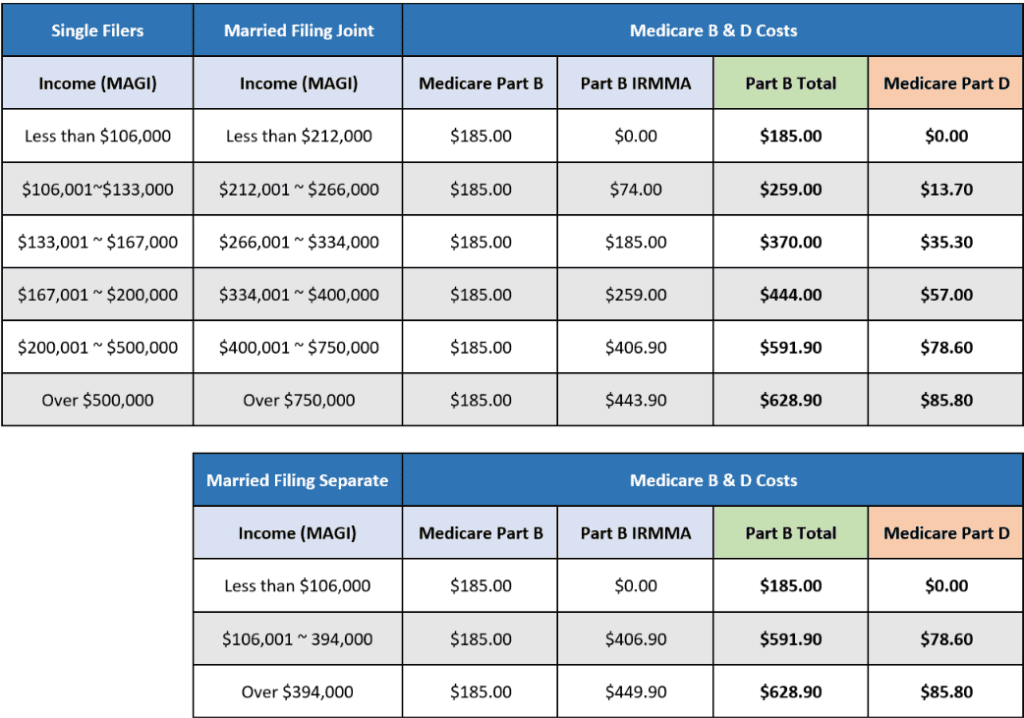

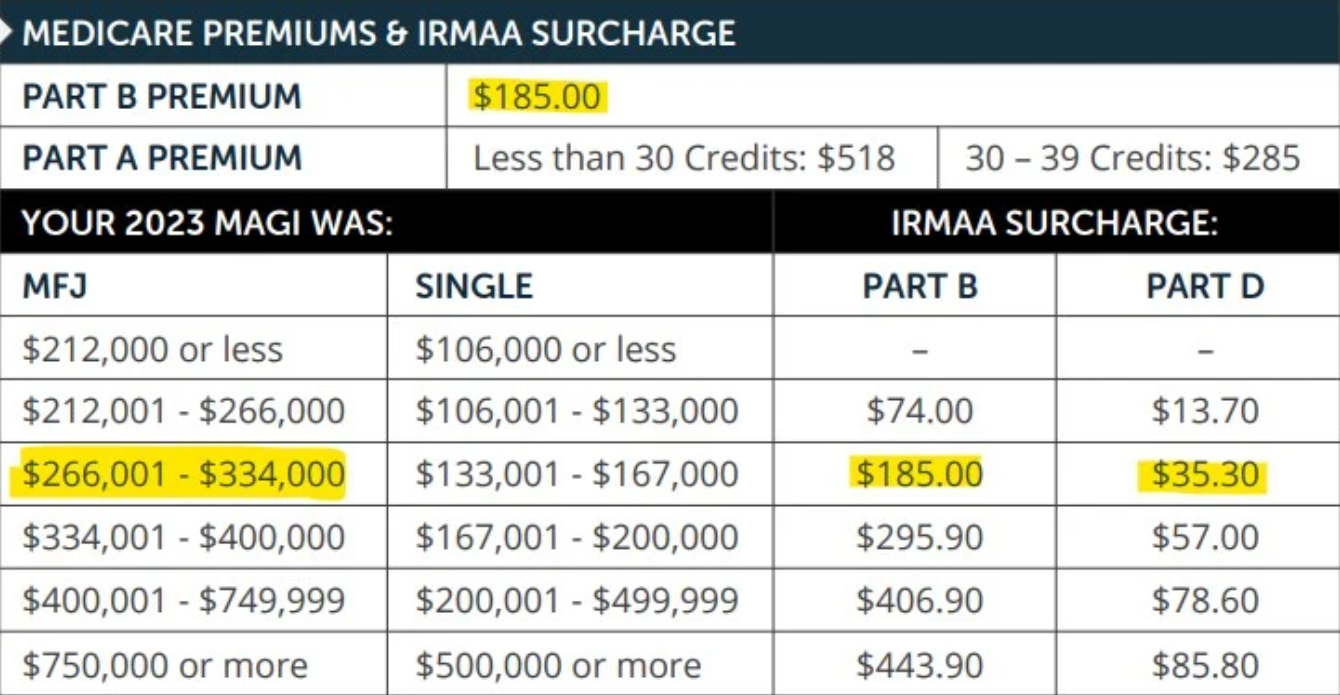

How IRMAA Actually Affects Medicare Costs

IRMAA operates in income tiers rather than gradual increases. Once income crosses a threshold:

- Medicare Part B premiums increase

- Medicare Part D premiums include an additional surcharge

- The increase applies for the entire year

- Each spouse is assessed individually

Because the surcharge appears years after the income decision, cause and effect often feel disconnected — even though the system is working exactly as designed.

IRMAA Is a Coordination Problem, Not a Tax Problem

IRMAA is often described as a “tax penalty,” but that framing misses the point.

The issue isn’t simply how much tax you pay.

It’s when income is recognized and how decisions interact over time.

A withdrawal today affects:

- Taxes this year

- Medicare premiums two years from now

- Flexibility for future income decisions

Viewed this way, IRMAA isn’t a problem to “optimize away.” It’s a signal that income, taxes, and benefits are interconnected — and need to be considered together.

Can IRMAA Be Avoided?

Sometimes. But more importantly, it can be anticipated.

In many retirements:

- Paying IRMAA temporarily may be acceptable

- Avoiding it entirely may not be realistic

- The real risk is being surprised by it

A coordinated approach doesn’t aim to eliminate every surcharge. It aims to make trade-offs visible before decisions are made.

Why This Matters for Retirement Confidence

Unexpected Medicare premium increases can:

- Disrupt monthly cash flow

- Create frustration and distrust in the planning process

- Undermine confidence in retirement income sustainability

When income, taxes, and Medicare are coordinated together, IRMAA becomes:

- Predictable

- Understandable

- Manageable within the broader retirement framework

How This Fits Into the Bigger Picture

IRMAA is one example of a broader reality in retirement:

Spending stability depends less on individual decisions and more on how those decisions are coordinated over time.

That includes:

- How you draw income

- When income is recognized

- How taxes and benefits interact

- How today’s choices shape future flexibility

Understanding IRMAA is a starting point. The next step is understanding how retirement income actually works — and why taxes play such an outsized role.

→ Next: How Retirement Income Really Works (and Why Taxes Matter More Than You Think)