Why Investment Returns Matter Less Than Income Coordination in Retirement

Investment returns dominate most retirement conversations.

They’re easy to quote, easy to compare, and easy to fixate on.

But once retirement begins, returns alone no longer determine how well retirement works. What matters more is how income, withdrawals, and taxes are coordinated as money moves from your portfolio into your life.

This is why retirees with similar portfolios can experience very different outcomes—even in the same market environment.

Returns Matter — Just Not in Isolation

Investment returns still matter in retirement. Growth helps portfolios last longer and supports spending over time.

What changes is how returns show up.

Once withdrawals begin:

- Returns interact with withdrawal timing

- Taxes affect how much return you actually keep

- Poor sequencing can magnify downside risk

- Good coordination can soften volatility

In retirement, returns are no longer the outcome. They’re one input in a larger system.

Why Returns Are a Blunt Tool for Measuring Retirement Success

Market returns tell you how an index performed.

They don’t tell you:

- Whether spending was sustainable

- Whether taxes spiked unexpectedly

- Whether income felt reliable year to year

- Whether flexibility was preserved

A retiree doesn’t experience the market.

They experience net spendable income.

That distinction matters.

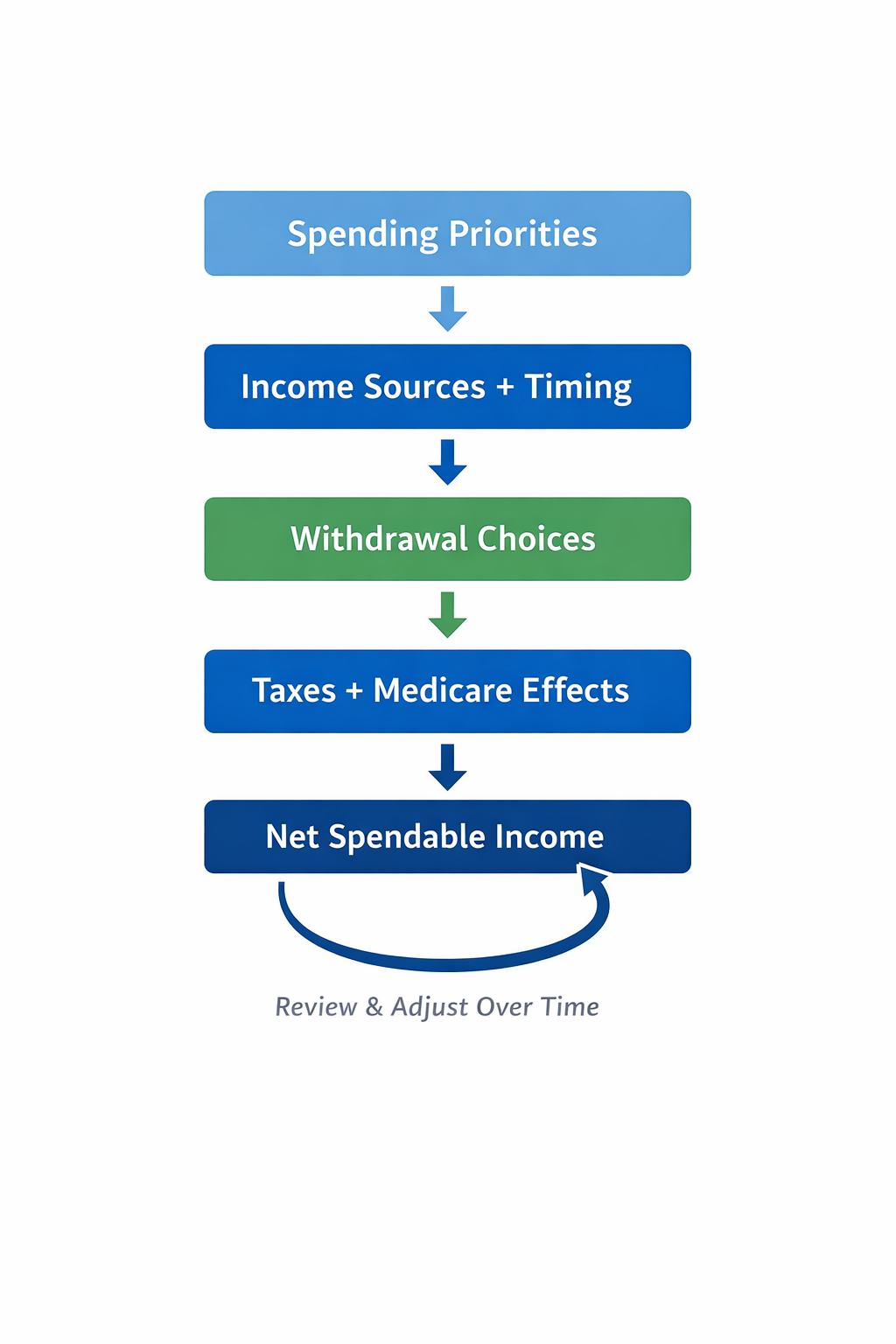

The Retirement Income Coordination Framework

Retirement works best when income, investments, and taxes are coordinated over time — not handled as separate projects. We use a simple framework: start with spending needs, map reliable income sources, coordinate withdrawal and tax decisions, and adjust as life, markets, and rules change. This approach helps keep retirement income steady and reduces surprises that often show up later.

This page focuses on why coordinating income, withdrawals, and taxes often matters more than maximizing investment returns.

How Coordination Changes the Role of Returns

When income decisions are coordinated:

- Market swings are absorbed more smoothly

- Withdrawals feel intentional rather than forced

- Taxes are easier to anticipate

- Spending adjustments feel manageable

When they’re not:

- Even strong long-term returns can produce uneven income

- Market downturns feel sharper

- Flexibility disappears faster than expected

The difference isn’t performance—it’s structure.

Sequence and Timing Often Matter More Than Performance

Two portfolios with identical long-term returns can produce very different retirement experiences depending on:

- When withdrawals occur

- Which accounts fund spending

- How taxes stack over time

- Whether adjustments are proactive or reactive

This is why coordination often outweighs marginal differences in returns, especially in the first decade of retirement.

Why Chasing Returns Can Increase Risk in Retirement

In accumulation, higher returns generally mean faster progress.

In retirement, chasing returns can:

- Increase volatility at the wrong time

- Force withdrawals during market stress

- Reduce income reliability

- Narrow future options

Retirement risk is less about average returns and more about how outcomes align with spending needs over time.

What a Coordinated Approach Prioritizes Instead

A coordinated retirement income approach prioritizes:

- Reliable cash flow

- Spending flexibility

- Tax awareness over time

- Adaptability as conditions change

Returns still matter—but they serve the system rather than driving it.

Bringing the Series Together

Across this series, one idea repeats:

- IRMAA shows how income timing affects Medicare costs

- Retirement income mechanics explain why taxes matter more than expected

- Withdrawal sequencing shows how decisions shape flexibility

- Returns vs. coordination explains why structure beats headlines

Each topic is different.

The framework underneath them is the same.

Where This Leaves You

A successful retirement isn’t built on a single decision or a single metric. It’s built on coordinated decisions made over time, with room to adjust as life unfolds.

That’s what keeps income steady—even when markets, tax rules, and priorities change.