How Retirement Income Really Works

(And Why Taxes Matter More Than You Think)

Retirement income is often misunderstood as a simple replacement for a paycheck.

In reality, it works very differently.

Once work stops, income doesn’t arrive automatically. It has to be assembled, year after year, from multiple sources—each with its own rules, tax treatment, and downstream effects. How those pieces are coordinated matters far more than most retirees expect.

This is why two households with similar savings can experience very different outcomes in retirement.

Retirement Income Is Assembled, Not Earned

During your working years, income is straightforward:

- You earn wages

- Taxes are withheld

- What’s left is available to spend

In retirement, income works differently. It may come from:

- Social Security

- Pensions

- Withdrawals from retirement accounts

- Taxable investment income

- Required minimum distributions

- One-time liquidity events

Each source behaves differently. Each is taxed differently. And each interacts with the others in ways that aren’t visible on a single statement or a single tax return.

The Real Complexity Is Timing, Not Amount

Most retirees focus on how much they can withdraw.

The bigger issue is when income is recognized.

Two retirees can spend the same amount and see very different results depending on:

- Which accounts fund spending

- Whether income is taxable, partially taxable, or tax-free

- How withdrawals overlap with Social Security or pensions

- Whether income crosses thresholds that affect taxes or Medicare

This timing effect is why retirement income decisions echo forward—sometimes years into the future.

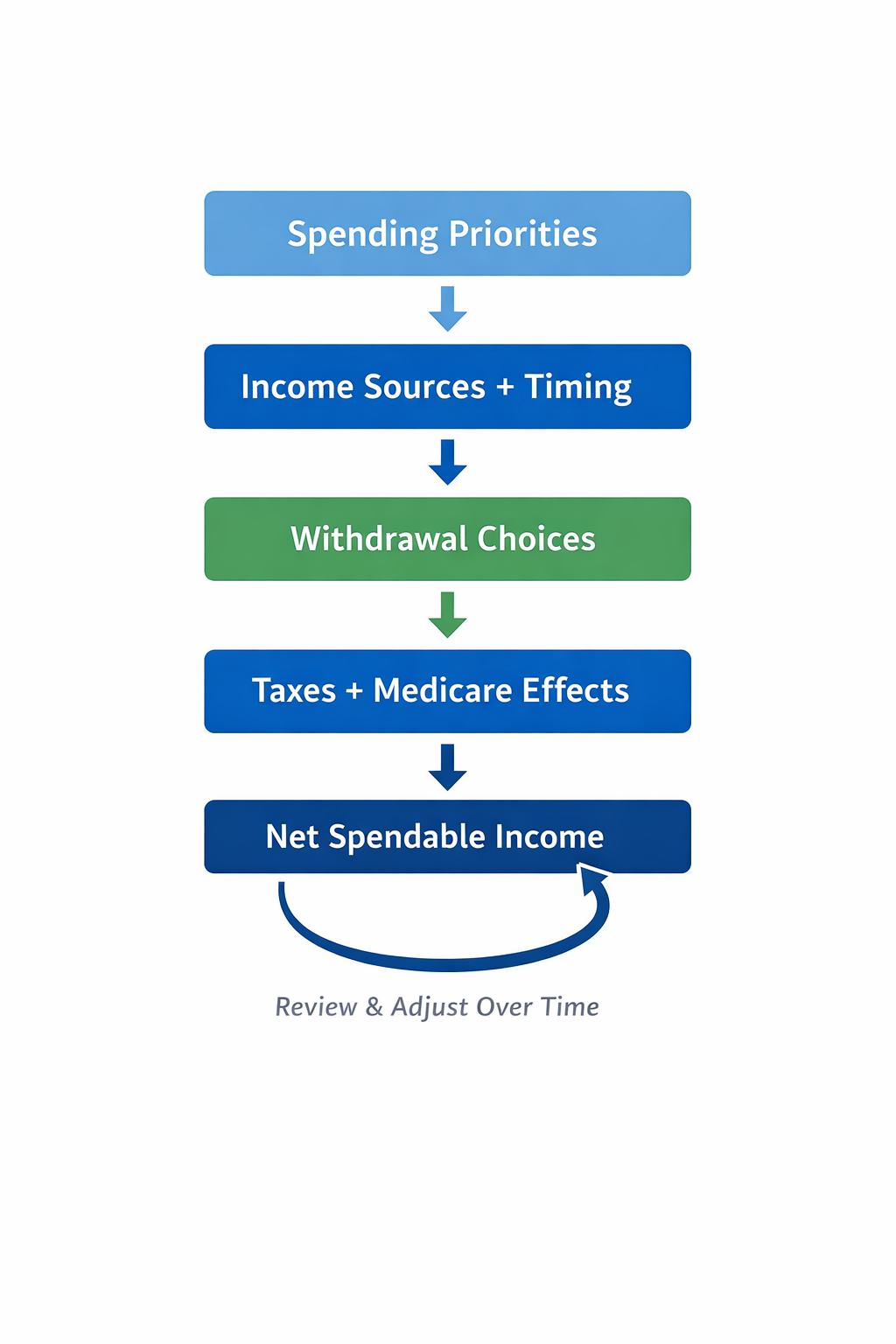

The Retirement Income Coordination Framework

Retirement works best when income, investments, and taxes are coordinated over time — not handled as separate projects. We use a simple framework: start with spending needs, map reliable income sources, coordinate withdrawal and tax decisions, and adjust as life, markets, and rules change. This approach helps keep retirement income steady and reduces surprises that often show up later.

This page focuses on how retirement income is assembled over time and why tax treatment matters more than most people expect.

Taxes Are the Throughline

Taxes aren’t a side issue in retirement. They’re the connective tissue.

They affect:

- How much income your portfolio can sustain

- How long assets last

- Whether benefits and premiums remain stable or become volatile

Unlike during working years, retirement taxes are often driven by your own decisions—not withholding tables. Withdrawals, conversions, and timing choices all shape the outcome.

This is also why focusing only on “this year’s tax bill” can lead to problems later.

Why “Tax-Efficient” Doesn’t Mean “Lowest Tax Bill”

It’s natural to want to minimize taxes each year.

In retirement, that instinct can backfire.

Minimizing taxes in one year can:

- Increase taxes later

- Trigger Medicare premium surcharges

- Reduce flexibility when circumstances change

A more durable approach looks at tax behavior over time, not year-by-year optimization. The goal isn’t to eliminate taxes—it’s to avoid avoidable surprises and preserve flexibility.

This is exactly how surprises like IRMAA show up.

→ Related: Understanding IRMAA: Why Medicare Premiums Surprise Retirees

Spending Is the Output, Not the Input

In retirement, spending isn’t a fixed number you lock in.

It’s the result of how income sources, markets, and taxes interact.

Sustainable spending depends on:

- Portfolio behavior

- Withdrawal patterns

- Tax interactions

- Benefit timing

That’s why effective retirement income planning emphasizes:

- Guardrails instead of rigid rules

- Adjustments instead of forecasts

- Flexibility instead of precision

The goal isn’t to predict the future perfectly. It’s to remain resilient as conditions change.

Why This Is Different From Accumulation Planning

Accumulation planning focuses on:

- Saving more

- Maximizing returns

- Growing account balances

Retirement income (Decummulation planning focuses on:

- Drawing income intentionally

- Coordinating tax exposure

- Preserving options over time

The shift from saving to spending is more than psychological—it requires a different way of thinking about decisions and trade-offs.

Coordination Beats Optimization

You can’t optimize retirement income one decision at a time.

A Roth conversion affects:

- This year’s taxes

- Medicare premiums later

- Future withdrawal flexibility

A withdrawal decision affects:

- Portfolio longevity

- Tax brackets

- Benefit interactions

Seen this way, retirement income is less about picking the “best” move and more about aligning decisions so they don’t work against each other.

How This Leads to Withdrawal Sequencing

Once you understand how retirement income actually works, the next question naturally follows:

How should withdrawals be structured over time so income remains reliable and flexible?

That’s where withdrawal sequencing comes in.

→ Next: Withdrawal Sequencing Explained: How Retirees Pay Themselves Over Time