The Retirement Income Coordination Framework™: Why Retirement Is Not a Portfolio Strategy

Traditional retirement planning focused primarily on investment performance and withdrawal rates. Build a portfolio. Select an allocation. Estimate a sustainable percentage. Adjust annually.

But retirement is not sustained by returns alone.

Retirement unfolds over decades. Markets fluctuate. Tax laws change. Spending shifts. Health events occur. Income timing decisions compound. When spending, income sourcing, tax strategy, and investments are managed separately, friction builds — and friction erodes sustainability.

Successful retirement requires something more.

It requires coordinated decision-making — a structured system that aligns spending strategy, income design, tax sequencing, and investment alignment so they work together year after year.

That system is what I call The Retirement Income Coordination Framework™.

What Is The Retirement Income Coordination Framework™?

The Retirement Income Coordination Framework™ is a structured decision system built to coordinate the critical variables that determine retirement sustainability.

Retirement does not fail because of poor returns alone. It falters when spending, income sourcing, tax decisions, and portfolio structure are not designed to function together as an integrated system.

Retirement is not an investment problem.

It is a coordination problem.

The Hidden Flaw in Traditional Retirement Planning

Traditional retirement planning typically begins with a portfolio.

Allocation is set.

A withdrawal rate is estimated.

Taxes are projected annually.

Spending is assumed.

Each variable is optimized independently.

But retirement decisions are not independent.

Spending influences tax exposure.

Income sourcing shapes volatility risk.

Withdrawal sequencing determines lifetime tax drag.

Investment structure must support income design.

When decisions are made in isolation, structural tension develops. Over time, that tension erodes flexibility and sustainability.

This is not a question of competence.

It is a structural limitation of the traditional model.

Why Retirement Is Not a Portfolio Strategy

A portfolio manages volatility.

It does not coordinate the decisions that determine retirement durability.

A portfolio cannot coordinate spending guardrails, income sourcing shifts, tax sequencing, Roth conversion timing, Required Minimum Distribution strategy, Social Security integration, or dynamic life adjustments.

Performance alone does not stabilize retirement.

One of the structural limitations of a portfolio-only approach is its exposure to sequence of returns risk — where the timing of market declines, particularly when income depends on portfolio withdrawals, can significantly impact long-term income sustainability.

Structure does.

A portfolio is a tool.

It is not the governing system.

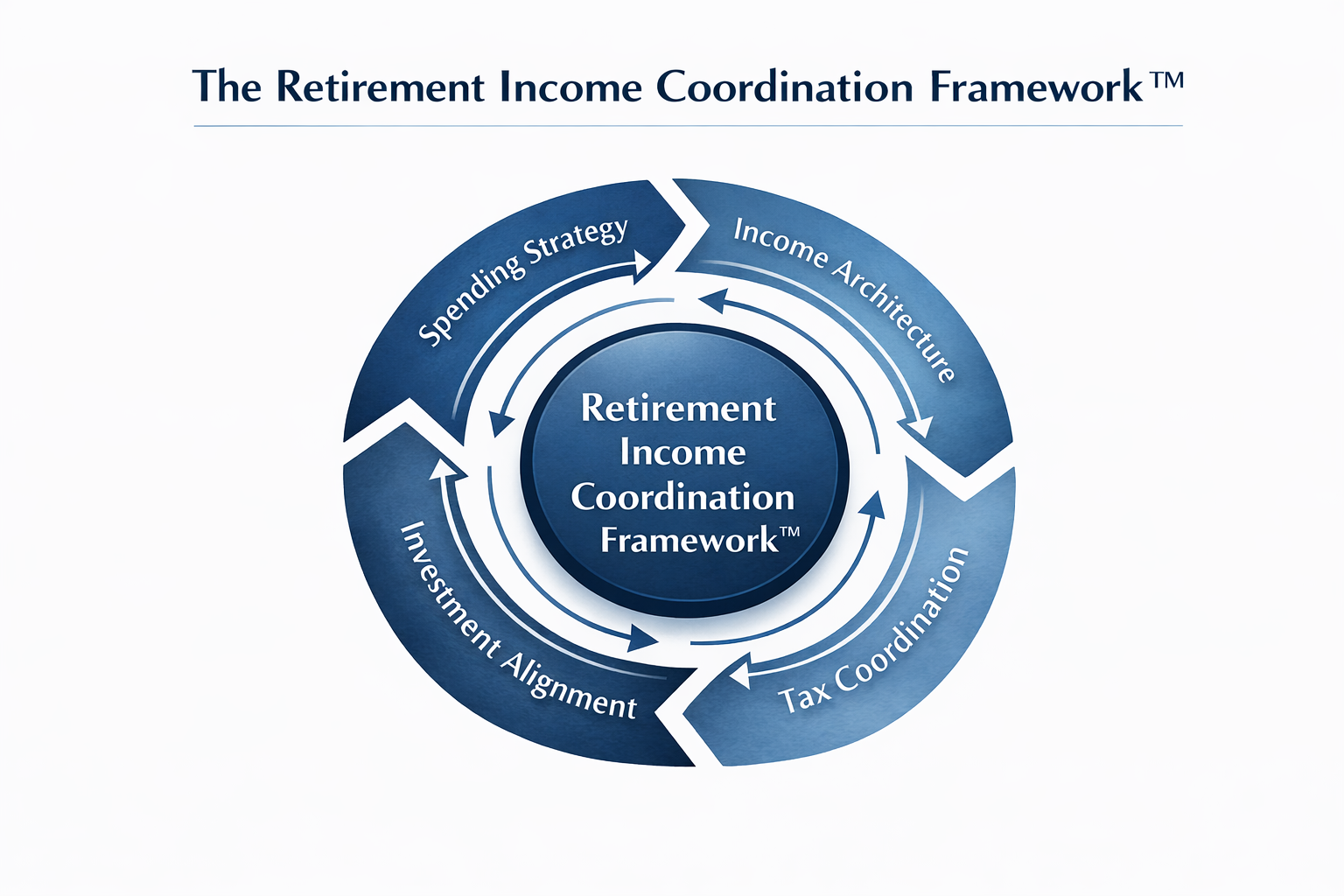

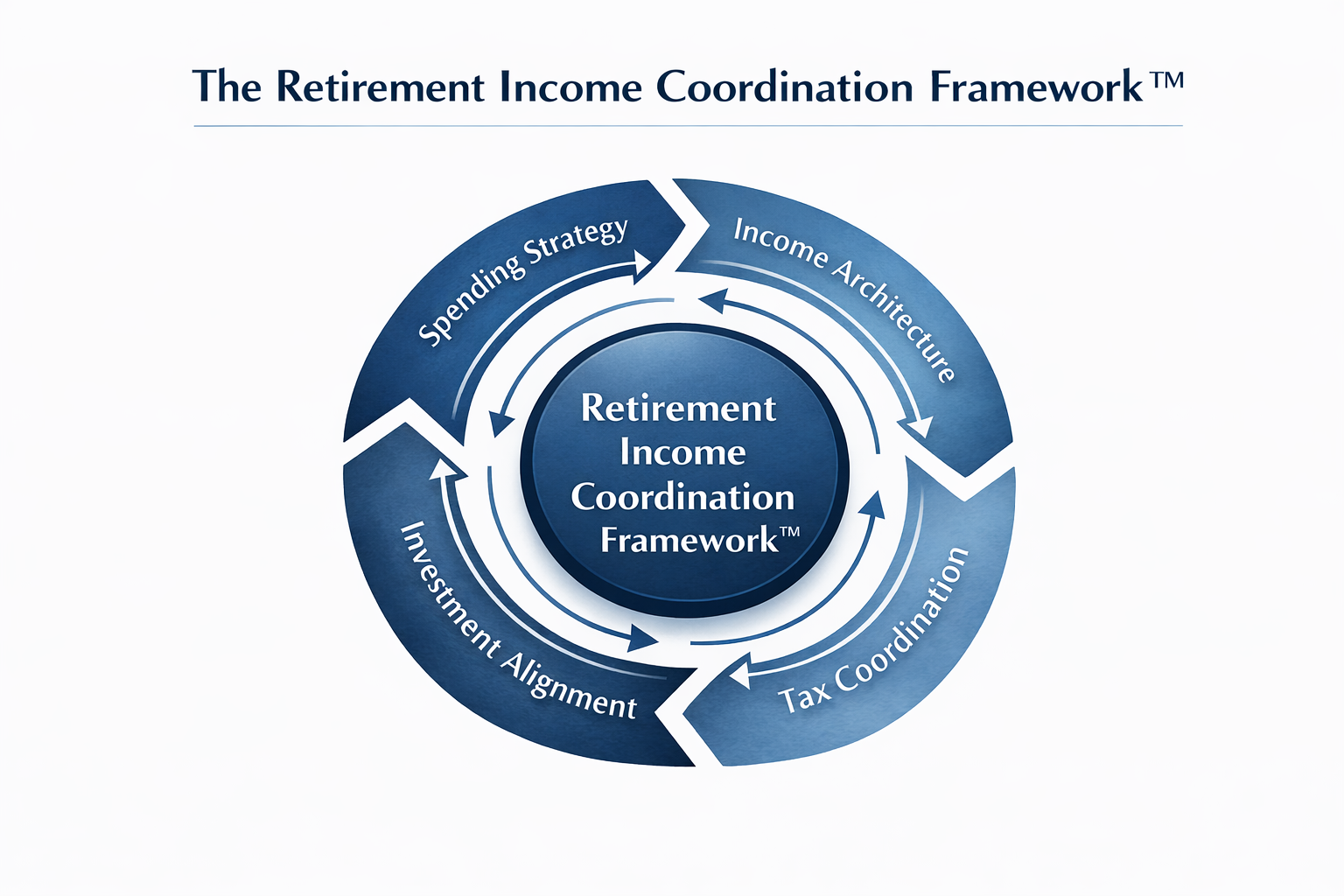

The Four Interdependent Pillars of Coordinated Retirement

The Retirement Income

Coordination Framework™ integrates four interdependent pillars. These are not services. They are decision systems designed to function together.

1. Spending Strategy — The Guardrails That Drive Every Decision

Retirement begins with spending clarity.

Defined guardrails establish sustainable ranges that adapt to market conditions and life changes. Without guardrails, income sourcing becomes reactive, tax strategy becomes inefficient, and portfolios absorb unnecessary strain.

Spending is not the outcome of retirement planning.

It is the driver of it.

2. Income Architecture — Designing How Income Is Sourced

Income sourcing is the structural engine of retirement design.

Some households prioritize stability.

Others prefer flexibility.

Some value protected income structures.

Others accept variability for long-term efficiency.

These preferences determine how income flows — and how risk is absorbed.

Income Architecture influences tax exposure, portfolio construction, behavioral resilience, and sustainability during market stress. When income is architected deliberately, volatility becomes manageable rather than destabilizing.

Well-designed income structure stabilizes the entire system.

3. Tax Coordination — Protecting After-Tax Spending Power

Retirement taxes are not an annual event.

They are a lifetime design variable.

Withdrawal sequencing affects marginal brackets, Medicare premiums, Social Security taxation, and long-term conversion opportunities. Decisions made early in retirement compound for decades.

The objective is not to minimize taxes this year.

It is maximizing after-tax spending power over a lifetime.

Tax coordination must operate in tandem with income sourcing and spending guardrails — not independently of them.

4. Investment Alignment — Supporting the Architecture

Investment strategy should follow income structure.

Not the reverse.

If income design prioritizes stability, portfolio structure must reinforce that objective. If flexibility is central, liquidity and total return efficiency must align accordingly.

Asset allocation supports the system.

It does not define it.

When portfolios are built first, and income is layered on top, misalignment follows. When portfolios are constructed to support Income Architecture, integration replaces tension.

Why Income Architecture Sits at the Center

Income sourcing shapes the retirement experience more than any other design decision.

It determines how volatility impacts spending.

It influences when tax opportunities can be captured.

It governs how guardrails adjust during downturns.

It dictates how investments must be structured.

Income Architecture is not a product decision.

It is a structural one.

And structure governs sustainability.

Retirement Is a Dynamic System — Not a Static Plan

Retirement unfolds over decades.

Markets fluctuate.

Tax laws evolve.

Spending patterns change.

Health events occur.

Family transitions reshape financial priorities.

A static plan cannot govern a dynamic system.

Coordination requires ongoing judgment — reviewing guardrails, reassessing income sourcing, evaluating tax opportunities, and confirming investment alignment as conditions change.

Sustainability is preserved through adaptation, not prediction.

What Coordinated Retirement Looks Like in Practice

During a market decline, the question is not, “What should the portfolio do?”

The question is, “How should the system respond?”

Guardrails are reviewed.

Income sourcing is reassessed.

Tax opportunities are evaluated.

Portfolio alignment is confirmed.

Multiple variables are considered simultaneously.

This is the difference between reacting to volatility and governing a coordinated system.

Who This Framework Is Designed For

The Retirement Income Coordination Framework™ is built for newly and recently retired households who recognize that retirement demands structure, not speculation.

It serves individuals who value disciplined decision-making, care about after-tax income, and understand that retirement sustainability depends on integration — not isolated optimization.

Retirement Is a Coordination System

Retirement success is not the optimization of one variable.

It is the disciplined integration of spending strategy, income architecture, tax coordination, and investment alignment — sustained over time.

When these pillars operate independently, instability compounds.

When they operate together, retirement becomes durable, adaptable, and structurally sound.

Retirement is governed by structure — not by forecasts.

And structure is built through coordination.