The Role of Predictable and Structured Income in Retirement

Explore how predictable and structured income fits into retirement and supports essential expenses within a balanced income framework.

Explore how predictable and structured income fits into retirement and supports essential expenses within a balanced income framework.

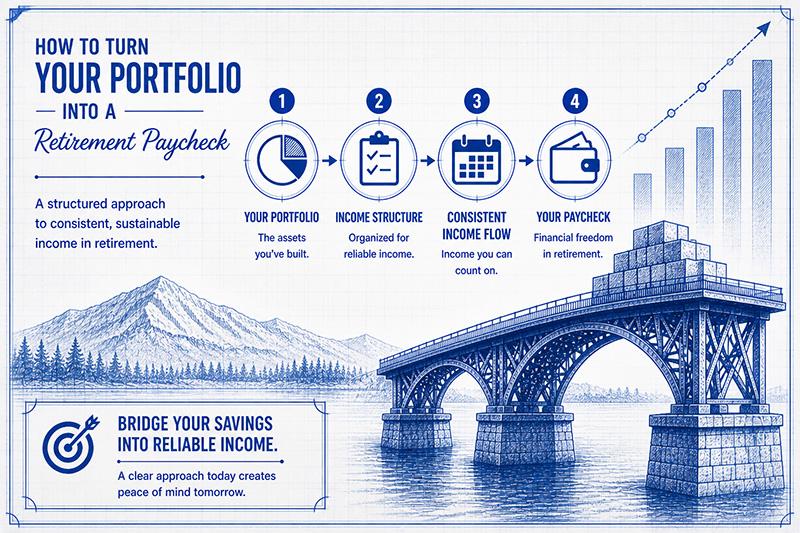

Learn how to convert your portfolio into a reliable retirement paycheck using structured income strategies and defined financial roles.

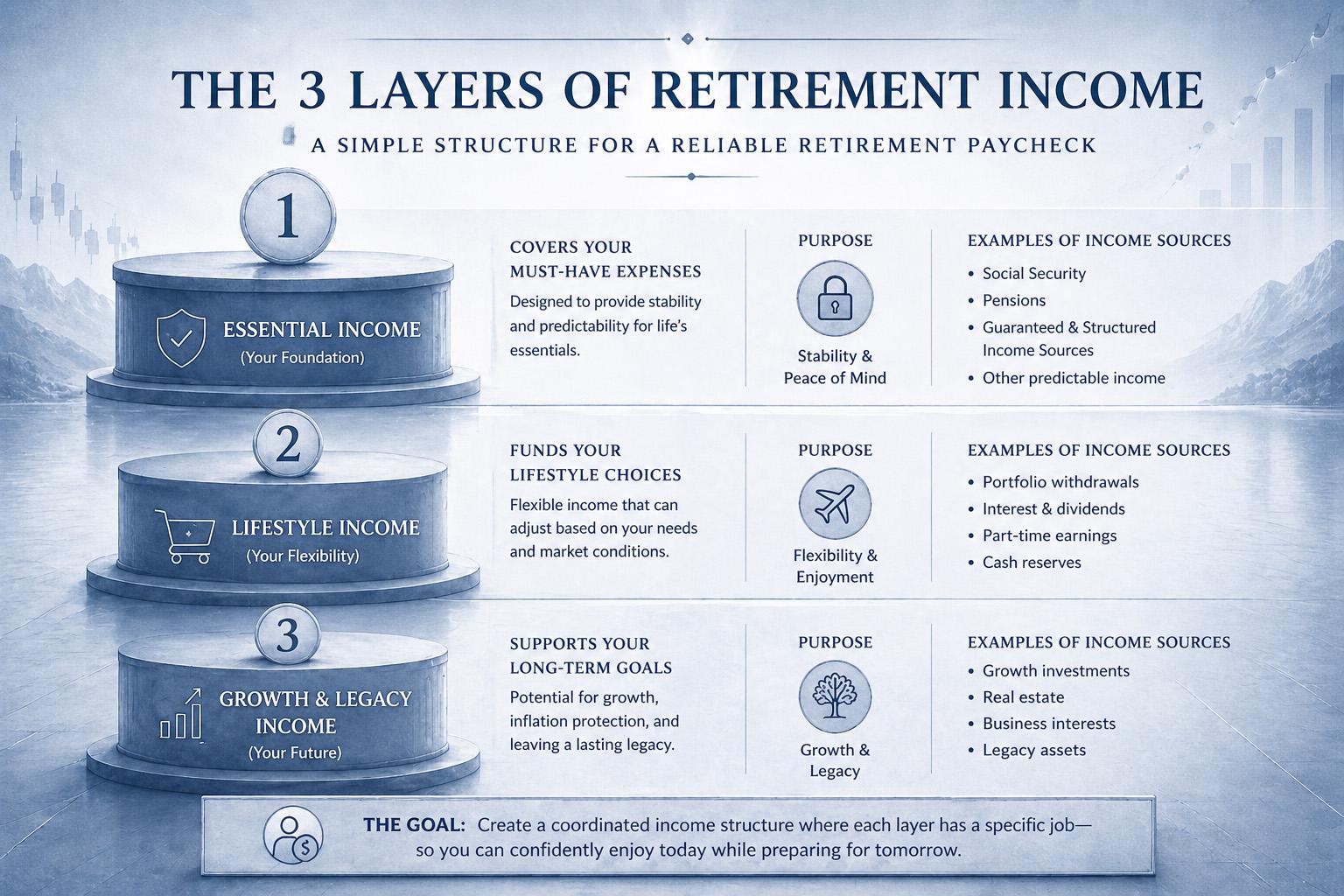

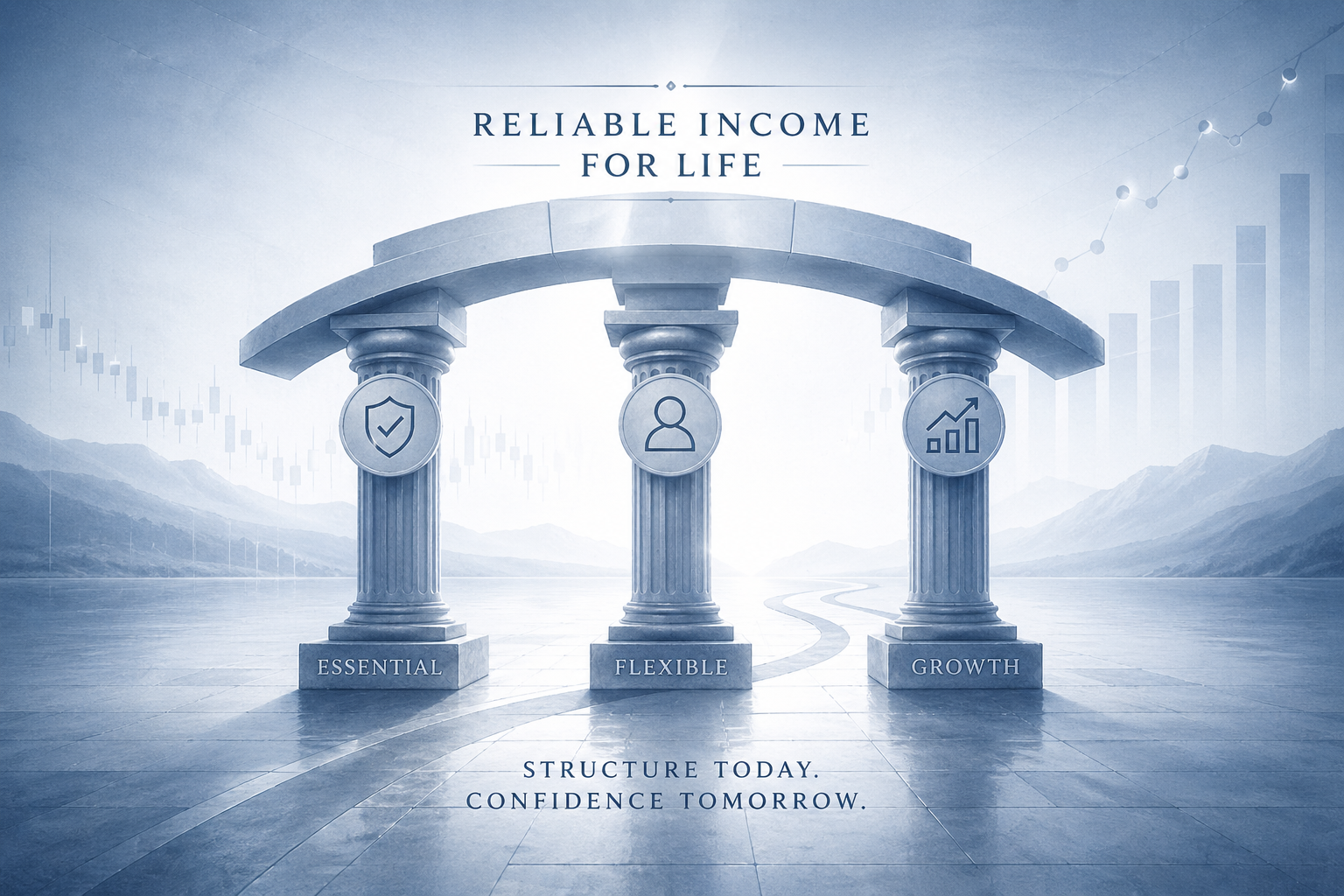

Understand the 3 layers of retirement income and how structuring income into defined roles can help create stability, flexibility, and long-term growth.

Learn how to turn your savings into a reliable retirement paycheck using a simple, structured income strategy designed for long-term clarity and confidence.

Not all spending creates the same level of risk. Some expenses must be covered no matter what, while others can adjust as conditions change. Understanding the difference between essential and discretionary spending is what allows you to create flexibility, maintain stability, and define sustainable spending in retirement.

The 4% rule is often seen as a safe withdrawal strategy—but it may introduce more risk than it removes. By relying on a fixed percentage, it ignores how markets behave, how spending evolves, and how decisions are made over time. A more effective approach focuses on defining sustainable spending with flexible guardrails rather than rigid rules.