The Efficient Retirement Newsletter (10-15-2020)

15-Minute Read

3 INSIGHTS FROM ME

I. Saving for and Spending in Retirement: Tax-Deferred vs. Tax-Free

Have you ever wondered where the best places to save and spend money in retirement are? Is it better to save to a tax-deferred or tax-free account while saving for retirement? And is it better to spend from tax-free accounts during retirement? I get it. It can be confusing, but as always, it depends! In this case, it depends on your current and future tax rates. Whether you are saving for or spending in retirement, tax rates matter greatly. That's because retirement savings accounts have different tax treatments that impact how much you'll pay in taxes now and later in retirement. While there are no hard and fast rules to determine the best places to save for and spend in retirement (as each person’s situation is different and future tax rates are almost impossible to predict), here are four general guidelines worth considering.

Guideline #1: Aim for tax diversification. Regardless of your tax rate, prioritize a savings strategy based on a mixture of taxable, tax-deferred, and tax-free accounts. This serves two purposes: create sources of tax-free withdrawals later in retirement and increase opportunities to grow tax-advantaged savings through reduced withdrawals. Ultimately, the goal is to accumulate a higher percentage of savings in tax-free accounts than in other account types.

Guideline #2: Save to tax-deferred accounts. When current tax rates are projected to exceed future tax rates, saving to tax-deferred accounts should be prioritized to get the deduction, reduce taxable income, and pay a lower tax rate at withdrawal. However, future withdrawals will be subject to more tax if tax rates rise.

Guideline #3: Save to tax-free accounts. When future tax rates are projected to exceed current tax rates, prioritize saving to tax-free accounts that accumulate tax-free and permit tax-free withdrawals when tax rates may be higher. It should be noted when current and future tax rates are estimated to be the same, saving to a tax-deferred or a tax-free account doesn’t matter from an after-tax amount standpoint.

Guideline #4: Convert taxes when in a lower tax bracket. Prioritize converting tax-deferred savings like IRAs, 401(k)s, and 403(b) accounts to Roth IRAs when current tax rates are lower than expected. Paying the conversion tax at lower rates will reduce taxes and hedge against future tax rate increases as withdrawals from Roth IRAs come out tax-free.

Regarding retirement planning, focus on the things you can control. One of which is where you save for retirement. Being informed about the tax nature of various saving account types and your current tax rate can help you make smart decisions, resulting in more money in your pocket to save for or spend in retirement.

II. Tax-Smart Retirement Savings for High-Income Earners

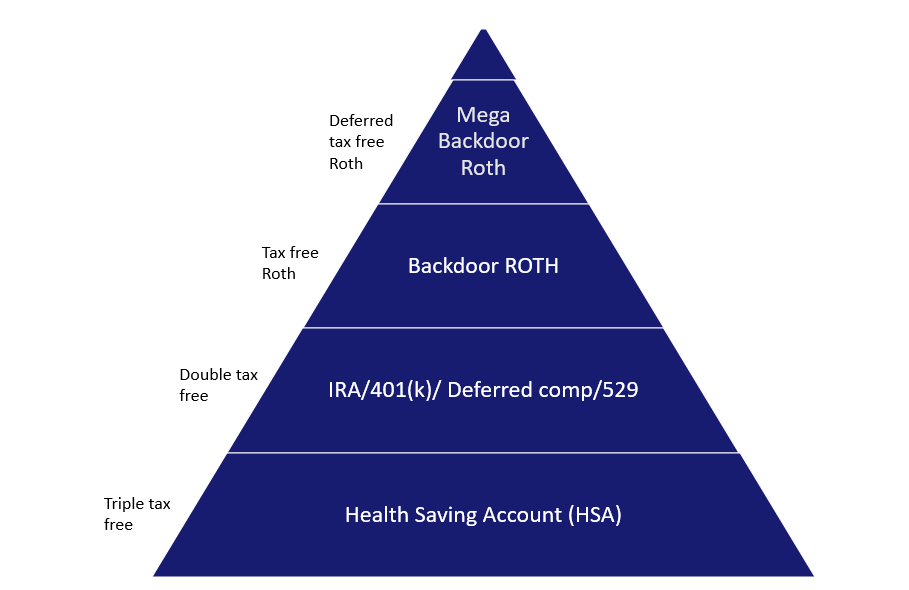

Saving for retirement can be challenging for all income earners, but more so for high-income earners. This is because they face restrictions on contribution amounts due to income limits on certain account types. The good news is that retirement saving choices for high-income earners aren’t limited to a 401(k), Roth IRA, or brokerage account. There are additional account types and strategies to use to maximize retirement savings. If you’re faced with this challenge, here’s a 4-step process to overcome the obstacles high-income earners face when saving for retirement in a tax-smart manner.

Step 1: Maximize 401(k). First, max out savings to a 401(k).

Step 2: Max out the Traditional IRA. If you’re ineligible to directly contribute to a Roth IRA due to a high income, you’ll want to contribute the maximum amount to a traditional IRA. You won’t be able to take a deduction due to high income, but that’s not the objective. The goal is to get money into the traditional IRA to set the stage for the next step.

Step 3: Backdoor Roth IRA. Your high-income level will not allow you to contribute directly to a Roth IRA, but there’s a strategy called a Backdoor Roth that will allow you to fund a Roth IRA by moving money from a traditional IRA to a Roth IRA. It’s a simple 3-step process where you withdraw the money from the tax-deferred accounts, pay the tax, and roll the funds into a Roth IRA. There are no limits on the amount to be converted. That is, anyone can convert any money from a traditional IRA/401k (assuming you are no longer contributing to the 401k plan) to a Roth IRA.

Step 4: Backdoor Roth IRA Savings. If you like the idea of a Roth IRA, you’ll fall head over heels for the supersize version, known as a mega backdoor Roth. This strategy works best with 401(k) plans that allow either in-service distributions to a Roth IRA — that is, you can take money out of the 401(k) plan while you’re still working at the company — or lets you move money from the after-tax portion of your plan into the Roth 401(k) part of the plan.

Don’t let high income stand in the way of increased retirement savings. Adopting this 4-step strategy will help you boost savings now and increase retirement income later.

III. 5 Keys to Increase Portfolio Longevity

We know that meeting spending goals and managing risks largely depend on the sustainability of assets. Measures taken to increase portfolio longevity are paramount for retirements that depend on generating income through portfolio withdrawals. These measures generally take the form of dynamic withdrawals, increased stock allocation, delayed Social Security claiming, variable spending levels, and integrating home equity. Together or separately, they work to extend the life of a portfolio. Let’s review each in more detail to understand their role in the longevity of your retirement portfolio.

Dynamic Withdrawals. Market volatility is an ever-present danger to any portfolio, but none more so than during retirement. This is because withdrawing from a depressed portfolio, especially early in retirement, raises the percentage of remaining assets withdrawn to unsustainable levels. An income strategy based on a market-sensitive withdrawal can adjust the withdrawal rate to a sustainable level to prevent portfolio depletion.

Increased Stock Allocation. Contrary to popular belief, holding a decreasing amount of stock in retirement can shorten the life of a portfolio. This is because a low stock exposure will not produce returns at the levels needed to keep pace with inflation (i.e., cost of living increases). Left unchecked, inflation will cause ever-larger withdrawals from the portfolio to meet spending needs, thus shortening the portfolio lifespan. The good news is stocks are the one investment proven to provide the returns needed to blunt the impacts of inflation. Recent studies suggest a steady or increasing stock allocation in retirement in the vicinity of 50% to 75% is superior to a declining stock allocation strategy.

Delaying Social Security. Postponing your Social Security claiming age to 70 increases lifetime benefits, produces more inflation-protected income, reduces portfolio withdrawals, and increases opportunities to build tax diversification. Of these benefits, reducing portfolio withdrawals is one of the most beneficial concerning portfolio longevity. That’s because a higher Social Security benefit requires lower withdrawals from the portfolio, as more money outside the portfolio is available to meet income needs. Delaying Social Security claiming age to 70 can increase the monthly benefit amount by 76% versus claiming early at 62.

Variable Spending Levels. According to a study done by Morningstar, assuming level spending over retirement overstates income needs and shortens portfolio longevity. Instead of a steady spending level through retirement, spending resembles a “smile” pattern, where spending is highest during the first ten years, lowest over the following ten years, and rises again late in retirement. Variable spending in retirement can increase the life of a portfolio.

Integrating Home Equity. Except for the wealthiest demographic, home equity represents 2/3 of retirement assets. This stat highlights that making smart decisions about how to integrate home equity into a retirement income plan may be more important than deciding how to invest and distribute other financial assets. These decisions can include spending home equity to extend the life of a portfolio. Studies show that spending from home equity can first increase spending and legacy as the portfolio is given more time to grow as spending is supported by other income sources such as Social Security and home equity.

When incorporated into a retirement financial plan, these five keys can extend the life of a portfolio to support spending goals and manage risks, leading to a more secure and fulfilling retirement.

2 FINDINGS FROM OTHERS

I. How to Mitigate Inflation Risk in a Retirement Income Plan

Retirement efficiency and managing inflation go hand in hand. This is chiefly since increasing expenses lead to increased withdrawals and quicker portfolio depletion. In this article, Jamie Hopkins, the Director of Retirement Research and Managing Director of Carson Coaching outlines a number of steps to implement to ensure your retirement income plan can withstand the effects of inflation. Those steps include increasing the portfolio stock allocation to hedge the impact of inflation, delaying Social Security to increase the amount of inflation-protected retirement income, purchasing annuities with the cost of living increase features to hedge price increases, or working longer as salary increases generally keep pace with inflation.

Source: How To Mitigate Inflation Risk In A Retirement Income Plan

II. What is an RICP, and Why Should Retirees Care?

Retirement income planning is much more complex than retirement saving planning. That’s because the strategies people need to use in retirement are very different from those used to build their nest eggs. The challenges of building a retirement income plan require retirees to find answers to questions like how to convert savings into steady retirement income, choosing when to claim Social Security and company retirement benefits, addressing health and long-term care, and more.

According to Dave Littell, the Retirement Income Program Director at the American College, retirees and near-retirees must consider partnering with a financial advisor knowledgeable in retirement income planning to ensure all goals are met and risks managed as efficiently as possible. Retirees should look for a financial planner with an RICP designation, so they’ll know their adviser has specific education and knowledge to guide them through all the complexities of making their savings last throughout retirement.

Retirees and soon-to-be retirees need to pick well-trained, educated, and qualified financial planners to help develop their retirement income plan. Moreover, financial planners with the RICP designation are in the best position to help you create a retirement income plan but also help build an efficient retirement income plan. These plans not only help retirees make sure their nest eggs last and have greater peace of mind during a retirement that could span decades but do so in the most efficient manner possible. Higher efficiency equates to more spending and more legacy.

Source: What is an RICP, and Why Should Retirees Care?

1 ACTION FOR YOU

I. Is Your Retirement Income Planning the Most Efficient?

Efficient retirement income planning begins with identifying and implementing the actions necessary to support your goals while protecting against risks that stand in the way of those goals. Undertaking the right actions consistently before and during retirement is crucial to your golden years.

We’ll look at one action item to take and reveal a new one each month.

This month’s action: Is your retirement income planning the most efficient? Not all retirements are created equal. Some cost more than others. And some cost more than they should. How do you know your retirement is costing you more than it should? A good starting point is thinking through a few questions to understand where your retirement income planning stands on the retirement efficiency continuum.

Here are a few questions to consider:

What will retirement cost? You’ll never know how much you need to save or can safely spend if you don’t know how much it will cost. Without a rough cost estimate, you’ll run the risk of oversaving, which isn’t efficient savings.

How do you manage income stability? Are you setting aside too many several assets to maintain a level of spending? Higher-than-needed savings to make up for spending reductions reduces assets available for other goals like lifetime spending, unexpected contingencies, and legacy.

How do you plan to manage outliving your assets? No one knows how long retirement will last. How will you deploy your assets to last for a retirement that could span multiple decades?

Are you projected to have a higher-than-expected tax liability? Are you incorporating efficient planning strategies such as tax-smart withdrawals, investment diversification, Roth conversions, and Social Security and Medicare benefit protection schemes? If your retirement income plan doesn’t include tax planning, you’re leaving quite a bit of money on the table.

WHAT'S NEXT?

Have a Question? Want to chat about it?

Until next month,

Mark Sharp, CFP® RICP® EA